Funding Urban Infrastructure: Value Creation, Property Tax and Other Revenues - Dominique Bureau

←

→

Transcription du contenu de la page

Si votre navigateur ne rend pas la page correctement, lisez s'il vous plaît le contenu de la page ci-dessous

Conseil

économique pour

le développement

durable

Funding Urban Infrastructure:

Value Creation, Property Tax and Other Revenues

Dominique Bureau

Conseil économique pour le développement durable

www.developpement-durable.gouv.fr

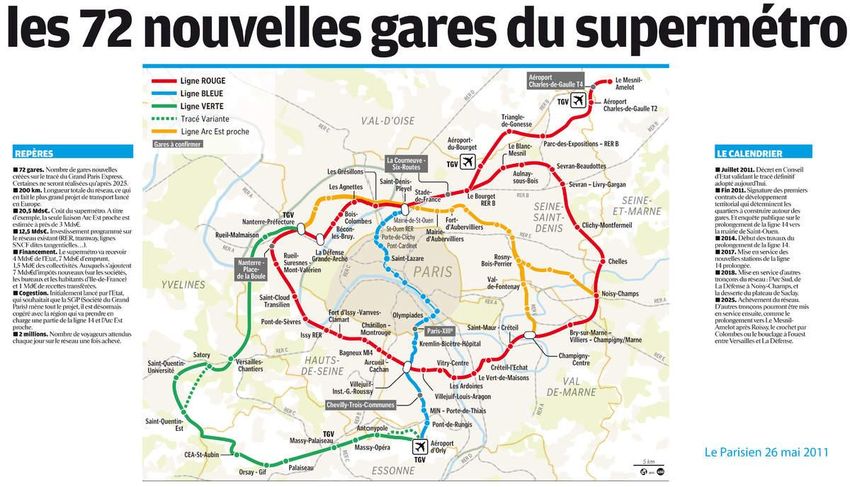

Motivation of the study: how to fund new stations…

Complex funding model

• Le périmètre des dépenses du Nouveau Grand

Paris d’ici 2030 est de 25,525 milliards d’euros.

• Pour financer ces dépenses, la Société du Grand

Paris dispose de recettes fiscales affectées déjà • Dans un deuxième temps, la SGP aura

mises en place, qui sont de trois natures :

recours à l’emprunt, qu’elle remboursera

– une fraction de la taxe locale sur les

bureaux en Île-de-France qui est assise sur grâce à trois types d’apports:

les surfaces à usage de bureaux, de locaux – les recettes fiscales affectées;

commerciaux, de locaux de stockage, de

stationnement ; – les redevances d’usage payées par

– la taxe spéciale d’équipement, taxe les exploitants (péages) à compter

additionnelle aux taxes locales ;

– une composante de l’Imposition des mises en services;

Forfaitaire sur les Entreprises de – les recettes complémentaires tirées

Réseaux (IFER) assise sur le matériel

roulant exploité par la RATP. Ainsi, la SGP notamment de l’exploitation

perçoit plus de 500 millions d’euros de commerciale des gares (publicité,

recettes fiscales affectées par an. commerce, etc.) ou d’autres

• L’État apportera un soutien budgétaire à la

Société du Grand Paris à hauteur de 1 milliard services.

d’euros. De même, l’État demande que les

collectivités locales apportent 225 millions

d’euros.

• Enfin, des recettes fiscales affectées

supplémentaires pourront être mises en place à

compter de 2020, en accompagnement des

améliorations de desserte procurées par les

premières mises en service.

A common problem

• The Crossrail 1 project funding structure includes a substantial contribution

from two local sources:

– the Business Rates Supplement (BRS) was established in London specifically

to fund Crossrail 1 and is generating a steady flow of income that is being used

to repay debt raised to finance the project’s construction.

– the Mayoral Community Infrastructure Levy (Mayoral CIL) is a charge on

all new development in London. Its purpose is to contribute to the cost of

additional infrastructure required as a consequence of new homes, offices and

other buildings.

• In summary, the views of those consulted were that:

– the levy elements of the funding package (BRS and Mayoral CIL) had

worked well (in that the loans taken out for Crossrail 1 are forecast be repaid

on time or even early);

– the amounts raised by negotiating contributions from landowners on the

route have generated only a small proportion of the value of the scheme;

– and many land and property owners who have benefited most from the

project are not making a commensurate contribution to the project costs.”

How to fund the renovation of existing ones?

The standard economic recommandation • HGT: the value created by • In practice: special tools (TIF, LOCAL public equipments JPD), rather than general capitalizes into land rents development of property taxes • Additional rents should be • And controversies about: taxed for financing the – Distortionary impacts of associated fixed costs property taxes (« capital • (By the means of property taxes view ») the local Authority recovers the – The degree of capitalization rent she has created)

Are new business models for airports transferable?

Lost steps

A strong, controversial, tendancy…

…need to clarify regulatory models

(one till vs double-till)

But, before that, the objectives:

additional revenues or enlarged

quality range of services for consumers?Purpose of the study

• Two questions:

– Management rules for additional services provided by

local public equipments: 1st Best (LLH) Pricing or

Ramsey-Boiteux markups?

– Assignment of potential funding instruments between

property taxes, other local taxes (poll, housing),

revenues from shops and services?

• Main characteristics of the model: a standard urban

monocentric model…

– which does not assume perfect population mobility

between cities (possible incomplete land rent

capitalization of the benefits of the projects)

– with property tax base including the value of buildings

(hence acting as taxes on construction)Notations • Willingness-to-pay for the services provided by the equipment • Social value for a resident • Surplus of a resident • Costs of the equipment

Urban costs

Competitive equilibrium of land markets

Optimal policy with two fiscal instruments: α, τ

A urban platform

Local public

Equipment

(d) (z,Y)

N

α τ

Social Value

(k)

Landowners

Developers ResidentsUrban externalities

Summary of results

Structure of local taxes Markups above

Role of property taxes (appropriate) MSC

Benchmark: perfect mobility; no distorsion +++ 0

Imperfect capitalization 0

Construction choices incentives 0

Agglomeration externalities 0

Architectural externalities 0

Weight of low-mobile residents 0

Heterogeneous WTP - or ?

Cost incentives - 0

Fixed costs selection, high mobility

Fixed costs selection, low mobility - From average cost pricing to TIF, JPD…

Conclusion

• The benchmark for pricing additional activities offered residents by public equipments

should remain marginal cost even with distorsions and imperfect mobility of residents.

Local taxes remain the most natural tools for funding fixed costs, the development of new

revenues from retail activities firstly being to be conceived as an element of a strategy for

global value creation.

• Structure of local taxes

– Fiscal distorsions. Ramsey-Boiteux features combined with externalities internalization

prevail,

– Selection of socially justified equipments. The transposition of the “average pricing

rule” in this context is to earmark or capture property value induced by the project to

fund it: the conditionality that supplementary land rents need to be greater than

development costs lead to the efficient levels for all public and additional services

provided by the equipment. In this perspective tools to test and implement this condition

must be developed.

• Extensions: competitive issues; cooperation between networksVous pouvez aussi lire