Le Pétrole et son avenir ? Une approche pragmatique - Charles Thiemele - 3 Juin 2021 - Ampersand World

←

→

Transcription du contenu de la page

Si votre navigateur ne rend pas la page correctement, lisez s'il vous plaît le contenu de la page ci-dessous

Le Pétrole et son

avenir ?

Une approche

pragmatique….

Charles Thiemele – 3 Juin 2021

To : Aurelien SIX

CO2 taxes to reduce greenhouse gas (GHG) emissions.

Embryonic Growth Mature Aging

pre -1900s 1900 - 2000 2000 - 2050? Post 2050?

Où en-est– Discovery of International End-user switch to Low wind & PV LCOE

on petroleum

First steps in E&P

activities

combustion market

growth

Periods of cheap

oil promoted

electricty

Natural gas displacing

oil for generation

Storage-cost reductions

Electric vehicles

mandatory in large cities

aujourdhui ?

Beginnings of the Renewables sources

displacement of Aggressive CO2

refining industry penetration

wood and coal taxation

Figure 1: Oil industry maturity curve

• Les prédictions annoncent : la fin du pétrole et un • L’actualité :

nouveau monde sans pollution à l’horizon 20X0 ? • Annonce de la taxation du CO2

Quid du X0 ? • Votation en Suisse du 13 Juin ( loi sur le CO2)

• Les décisions du Mercredi 26 Mai – Black Wednesday

20 : Presque Business As Usual • Décision de la Cour Suprême Allemande pour 2050

30 : Peak Oil annoncé pour 2035 par certains experts • Prédictions post COVID

40/50 : Plus réaliste et en ligne avec les différents targets

!

Où en-est–

on

aujourdhui ?

• Le Syndrome du Black Wednesday….plus rien ne

sera plus jamais comme avant :

• La responsabilité des Boards

• Le concept du pollueur-payeur

• Les activistes sont écoutés et gagnent des

batailles

• La fin de la toute puissance du Big Oil ?

Quelles

influences ?

Renewable / Clean

Fossil Fuel based World 2035….2050

Energy based World

1/ Les lobbys ‘ verts’ :

Greenpeace

Greta Thunberg etc.

Accord de Paris ( COP…)

2/ Les anti-pétroles

3/ Les facteurs influenceursEmbryonic Growth Mature Aging

pre -1900s 1900 - 2000 2000 - 2050? Post 2050?

Quelles

influences ? Discovery of

petroleum

International

combustion market

End-user switch to

electricty

Low wind & PV LCOE

Storage-cost reductions

growth

First steps in E&P Natural gas displacing

Electric vehicles

activities Periods of cheap oil for generation

mandatory in large cities

oil promoted

Beginnings of the Renewables sources

displacement of Aggressive CO2

refining industry penetration

wood and coal taxation

1/ La demande Figure 1: Oil industry maturity curve

2/ La production

3/ Les facteurs internes :

* La reprise post-COVID

* La reduction des stocks

* La lenteur des investissements de conversion

3/ Les facteurs externes :

* Accords Opec / Opec +

* Les électrons libres : Iran / Lybie / Iraq / Nigéria etc. ( Géopolitique / Résolution des conflits)

* Les nouvelles productions : découvertes et investissements GreenfieldLa

demande?

1/ LA CONSOMMATION MONDIALE

LE FACTEUR LE PLUS IMPORTANT ET LE PLUS INFLUENT SUR LE MONDE DU PETROLE

* IL IMPACTE LE PRIX PLUS QUE TOUT AUTRE FACTEUR - EX. MARS 2020

* C’EST LE DRIVER PRINCIPAL DE L’ACTIVITÉ ET CELUI VERS LEQUEL SE TOURNENT LES

GROS PRODUCTEURS ( PRIX, PART DE MARCHE ETC.)

SON EVOLUTION SUR LES PROCHAINES PÉRIODES DÉTERMINERA :

* LE PRIX DU PÉTROLE A MOYEN/LONG TERME

* LE COMPORTEMENT DE L’OPEC/OPEC+ ET DES GROS PRODUCTEURS

* LA DIMENSION DES INVESTISSEMENTS DANS L’UPSTREAM (-5% si 0 investissement )

* Entre $3T et $20T pour compenser la demande actuelle sur 30 ans

* L’IMPORTANCE RELATIVE DE CERTAINS PAYS ET CERTAINES ECONOMIES

* EXEMPLE : INDE / CHINE / ARABIE SAOUDITE

AUJOURD’HUI, ON RESTE DANS UN MONDE A PLUS DE 80% DE CONSOMMATION ‘OIL&GAS’The 10 largest oil1 producers and share of total world oil production2 in 20203

La

Country Million barrels per day Share of world total

United States 18.60 20%

Saudi Arabia 11.01 12%

Russia 10.50 11%

production?

Canada 5.29 6%

China 4.93 5%

Iraq 4.16 4%

United Arab Emirates 3.79 4%

Brazil 3.78 4%

2/ Quelques faits sur la production : Iran

Kuwait

2.81

2.66

3%

3%

Total top 10 67.52 72%

• Des découvertes importantes continuent….. World total 94.24

alors que l’on annonce la fin du Pétrole : elles sont nécessaires12 Oil

pour soutenir

includes crude oil, alllaother

demande.

petroleum liquids, and biofuels.

Production includes domestic production of crude oil, all other petroleum liquids, biof

processing gain.

• Investissements de plusieurs centaines de Milliards par3 Source:

an ! International Energy Statistics, Total oil (petroleum and other liquids) produc

The 10 largest oil1 consumers and share of total world oil consumption in 20182

• Les USA sont le premier producteur de pétrole et ….le premier consommateur :

Country Million barrels per day Share of world total

United States 20.51 20%

• Le comportement futur du conducteur américain est un facteur clé China

India

13.89

4.77

14%

5%

Russia 3.88 4%

Japan 3.79 4%

• Il reste encore beaucoup de barrils à sortir : Saudi Arabia 3.08 3%

Brazil 3.06 3%

South Korea 2.57 3%

• Régions sous-exploitées ou mal-exploitées Canada 2.53 3%

• Ralentissement dues au conflit et aux conjonctures défavorables Germany

Total top 10

2.33

60.40

2%

60%

World total 100.37

• Le critère de part de marché reste encore important pour de

1 Oilgrands producteurs,

includes crude notamment

oil, all other petroleum liquids, and biofuels.

les pays du Moyen Orient 2

Source: International Energy Statistics, Total oil (petroleum and other liquids) consumEmbryonic Growth Mature Aging

pre -1900s 1900 - 2000 2000 - 2050? Post 2050?

Les

Discovery of International End-user switch to Low wind & PV LCOE

petroleum combustion market electricty

Storage-cost reductions

growth

First steps in E&P Natural gas displacing

Electric vehicles

activities Periods of cheap oil for generation

fantasmes?

mandatory in large cities

oil promoted

Beginnings of the Renewables sources

displacement of Aggressive CO2

refining industry penetration

wood and coal taxation

Figure 1: Oil industry maturity curve

1/ Oil @ 200$

2/ Peak Oil – No more oil in 20X0

3/ No more cars

4/ Hydrogen Airplanes

5/ What else ?Embryonic Growth Mature Aging

pre -1900s 1900 - 2000 2000 - 2050? Post 2050?

Quelques

Indicateurs

Discovery of International End-user switch to Low wind & PV LCOE

petroleum combustion market electricty

Storage-cost reductions

growth

First steps in E&P Natural gas displacing

Electric vehicles

activities Periods of cheap oil for generation

Clés?

mandatory in large cities

oil promoted

Beginnings of the Renewables sources

displacement of Aggressive CO2

refining industry penetration

wood and coal taxation

1/ % of Non-fossil Fuel-based Consumption - Quel est1:leOilbon

Figure taux

industry ? curve

maturity

Chine – 15% en 2020 et 20% en 2030 – Plus grand producteur de EV au Monde ….mais aussi un

très gros consommateur.

2/ Rate of Decarbonization or Carbon Neutral Target

* Comment L’Atteindre et Quand ? 2030 ? 2050 ?

3/ Public Policy Enforcement

* Seul moyen de changer les comportements - Shell doit baisser ses emissions de 45% sur 10 ans

/ Plus de voitures à combustion en 2030/2040 etc.

4/ LCoE : Levelized Cost of Energy (LCOE)

* Avantage progressif à l’Hydrogène, au Solaire et à l’Éolien& storage (CCS) and batteries.

4 .3%

Wind

Solar

CCS

Que fait le

Biofuels, biomass & waste

Energy smart technologies

2.3%

1.8%

Big Oil? 1.3%

1.1%

0 .9%

0 .7%

0 .2% 0 .2% 0 .2% 0 .1% 0 .1%

ExxonMobil

1/ Plus d’investissements dans le

Marathon

Petrobras

Chevron

CNOOC

Repsol

Inpex

Shell

Equinor

Eni

Total

BP

Renewable

2/ Un accent fort sur le Solaire et le

Wind Figure 2: Disclosed low-carbon investments as a proportion of total

CAPEX (2010–Q3 2018) Source: Reuters

3/ Est-ce un vrai trend ou juste une

réponse à la pression ?

4/ Le Big Oil est-il le mieux placé pour

répondre aux problématiques de

conversion ?

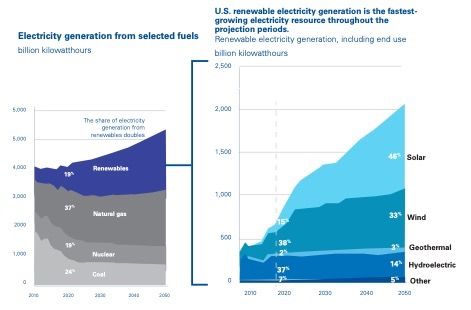

5/ What else ?Quid de Fossil focus All energy

l’avenir? Global

Trading houses

Global services co.

1/ La nécessaire transformation des sociétés du BIG Oil :

Independent retailers

XXL oil co.

Special-purpose vehicles

* La pression pour être dans le renewable ? Regional Energy

Mini-majors holding

* Pression politique / sociétale

* Divergences régionales et continentales ?

Local

* Quels investissements ? Pour quels résultats ?

American drillers

2/ Les nouveaux acteurs / métiers du Pétrole

Figure 4: Oil companies of the future ecosystem

3/ Les trends :

* Que voit-on maintenant ( 2020/2021) ? Outlining opportunities for expansion

* A quoi s’attendre ?

Regardless of its chosen business model, the oil company

of the future will find that opportunities for growth and• Oil consumption

Quid de

120

Mb/d

l’avenir? 100

80

• La barre des 100 Mb/d est-elle un vieux

souvenir ?

60

• A quelle Vitesse va-t-on revenir à 80 / 60 / 40 ?

40

Rapid

• Peut-on croire à un monde sans transport de

masse à combustion, sans voitures, sans énergie

Net Zero

‘sale’ ? Et si oui à quelle échéance 20

Business-as-usual

0

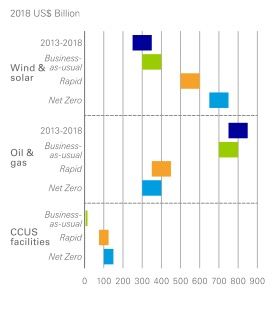

2000 2010 2020 2030 2040 2050Business As Usual

Quid de

l’avenir?

• BUSINESS AS USUAL

++ : TROP D’ÉCONOMIES A LA TRAÎNE

-- : CONSÉQUENCES DU BLACK WEDNESDAY

• RAPID

++ : PROGRESSION DU SOLAIRE ET DE

L’EOLIEN / INVESTISSEMENTS DANS LE

RENEWABLE

-- : HARMONISATION DES ACTEURS

• NET ZERO Rapid Net Zero

++ : MODÈLES BEST PRACTICE DES NORD-

EUROPÉENS

-- : LE MODELE COÛT/BÉNÉFICE RESTE À

PROUVEREmbryonic Growth Mature Aging

pre -1900s 1900 - 2000 2000 - 2050? Post 2050?

Ce que je

Discovery of International End-user switch to Low wind & PV LCOE

petroleum combustion market electricty

Storage-cost reductions

growth

First steps in E&P Natural gas displacing

Electric vehicles

activities Periods of cheap oil for generation

mandatory in large cities

oil promoted

Beginnings of the Renewables sources

crois?

displacement of Aggressive CO2

refining industry penetration

wood and coal taxation

Figure 1: Oil industry maturity curve

1/ 3 Mondes vont co-exister ….comme pour le COVID-19 :

* Les pays en avance sur le green energy : eliminer les combustibles et surtaxer le CO2 : objectif Carbon Neutral et Oil vers 20-40%

* Les pays en conversion prônant une gestion mixte – Reduire le Oil vers 60-70%

* les pays à la traîne : encore completement dépéndantes du Oil – Scenario BAU (BP) – Business as Usual – Oil au-dessus de 80%

2/ Passage du Tout Oil au Smart Oil : les politiques publiques vont pousser à déterminer ce qui fait sens pour les économies et les populations

de facon locale :

* Il est utopique de penser energie electrique dans des pays ou les delestages sont monnaie courante et ou les distances

necessitent l’utilisation de fossiles

* Par contre, la pression accrue sur le gaspillage des energies limitées vont encourager les best practices à se vulgariser ( Ex : La

Chine avec ses 400,000 Bus electriques – 3% sur la demande mondiale)

* Le COVID-19 a permis de rationaliser de facon interessante l’utilisation de l’avion.

3/ S’eloigner des fantasmes et rester pragmatique…..pas de syndrome papier toilette !ANNEXES

At present, European majors are — Chevron has a modest renewables — Royal Dutch Shell’s low-carbon

well ahead of U.S. companies in portfolio of around 65 MW, business plans include investing

the push toward renewables and designed to serve its core oil- between $2 billion and $3 billion

related utilities.35 The U.S. oil and and gas-producing operations.39 annually in wind and solar power

gas industry’s average investment The company recently entered a generation alone, with additional

in noncore areas, including green global power purchase agreement investment dedicated to EV

energy, has been around one percent (PPA) designed to “green” its charging, hydrogen and biofuels,

of total capital expenditure to date.36 power supply, which represents a and other clean energy innovation.

It’s no surprise that U.S. companies significant advance. The company The company’s incubator, Shell

have been more conservative, given has also invested $1 billion in Ventures, invests in and partners

investor expectations and other CCUS projects in Australia and with small and medium enterprises

challenges for even the very largest Canada, and, in 2018, launched a (SMEs) to develop new technologies

players in oil and gas. However, their US$100 million Future Energy Fund and business models.41

efforts are expanding. Examples to invest in innovative technology.40

— Total now has a gross low-carbon

across the globe include: The venture capital fund has

power-generation capacity of almost

targeted EV charging, battery

— BP announced a $1 billion 9 gigawatts worldwide, including 5

technology, and direct-CO2 capture

investment in offshore wind gigawatts from renewable energies

from the air.

projects through a deal with Equinor and a target of 25 GW of renewable

in September 2020 and is looking — ExxonMobil is investing more than generation by 2025.42 At the

to expand even further in North $1 billion per year into R&D-related beginning of 2020, the company

America. The move was part of to reducing carbon emissions, won Europe’s largest EV charge-

the company’s stated target of net and the company has a biofuels point contract in the Netherlands,

zero by 2050, including increasing output goal of 10,000 b/d by 2025. partnered with Groupe PSA in a

renewable power capacity to 50 The company has also invested pilot EV battery facility, and took a 2

GW over 10 years. The company heavily in carbon capture and GW Spanish solar position.43

already has a sizeable onshore wind storage (CCS) and discloses it has

business.37 BP has also partnered a working interest in approximately

in CCUS and hydrogen projects, one-fifth of the word’s total carbon-

among others.38 capture capacity.• Disruptive energy sources: Taking early positions in

development of innovative technologies such as fusion

or hydrogen sources.

Case example: Shell New Energies Case example: Total’s commitment to renewable energy

To play its part in creating a low-carbon future, Shell has

set up its New Energies business, with projects in biofuels,

biomass, hydrogen-fueling stations, EV charging, gas-to- Convinced of the opportunities renewable energies have

liquid (GTL)/liquefied natural gas (LNG), onshore and offshore

wind, thermal and photovoltaic solar, and power distribution to offer, Total is focusing its main ambitions on solar power

and electricity supply from renewable energy sources. The

company is planning to spend between $1 billion and $2

generation, targeting production capacity of five gigawatts

billion annually in the New Energies divisions until 2020. Even

though this represents less than 1 percent of revenues, it

by 2022. Other areas of focus are wind and hydraulic power

still positions Shell as one of the largest investors behind the

“energy transition”.

generation technologies. Total also believes optimizing

Case example: Equinor New Energy Solutions and

energy storage is key to expansion of renewables, which

Energy Ventures fund

is why it has acquired Saft, a world leader in battery

Equinor is also betting on developing non-traditional sources

of energy under its New Energy Solutions division. It has

technology. A further area of interest for Total is bioenergy,

become a significant innovator in offshore wind technology

and a world leader in carbon capture and storage (CCS)

in which commercial biomass production has allowed it to

technologies. According to Equinor, its Energy Ventures

fund is one of the world’s largest corporate venture funds

produce biofuels including ethyl tert-butyl ether (ETBE) and

dedicated to investing in attractive and ambitious growth

companies in renewable energy; it has earmarked more than

hydrotreated vegetable oil (HVO) for diesel.

$200 million in total investment capital.

Insight for the executiveFREQUENTLY ASKED QUESTIONS (FAQS)

What countries are the top producers and consum

FREQUENTLY ASKED QUESTIONS (FAQS)

of oil?

The 10 largest oil1 producers and share of total world oil production2 in 20203

What countries are the top producers and consum

Country

United States

Million barrels per day

18.60

Share of world total

20%

of oil?

Saudi Arabia

Russia

11.01

10.50

12%

11%

Canada

The 10 largest oil1 producers and share 5.29of total world oil production

6% 2 in 20203

China 4.93 5%

Iraq

Country 4.16 per day

Million barrels 4% total

Share of world

United

UnitedArab Emirates

States 3.79

18.60 20%4%

Brazil

Saudi Arabia 3.78

11.01 12%4%

Iran

Russia 2.81

10.50 3%

11%

Kuwait

Canada 2.66

5.29 3%

6%

Total

Chinatop 10 67.52

4.93 72%

5%

World

Iraq total 94.24

4.16 4%

United Arab Emirates 3.79 4%

1 Brazil

Oil includes crude oil, all other petroleum

3.78 liquids, and biofuels. 4%

2 Iran 2.81of crude oil, all other petroleum

3%

Production includes domestic production liquids, biofuels, and refin

Kuwait 2.66 3%

processing

Total top 10

gain. 67.52 72%

3 Source: International Energy Statistics, Total oil (petroleum and other liquids) production, April 1, 20

World total 94.24

The

1 Oil10

includes oil1 consumers

largestcrude and shareliquids,

oil, all other petroleum of total

andworld oil consumption in 20182

biofuels.

2 Production includes domestic production of crude oil, all other petroleum liquids, biofuels, and refiner

Country Million barrels per day Share of world total

processing gain.

United States 20.51 20%

3 Source: International Energy Statistics, Total oil (petroleum and other liquids) production, April 1, 202

China 13.89 14%

India 4.77 5%

The 10 largest oil1 consumers and

Russia 3.88

share of total world oil consumption

4%

in 20182

Japan 3.79 4%

Country Million barrels per day Share of world total

Saudi Arabia 3.08 3%

United States 20.51 20%

Brazil 3.06 3%

China 13.89 14%

South Korea 2.57 3%

India 4.77 5%

Canada 2.53 3%

Russia 3.88 4%

Germany 2.33 2%

Japan 3.79 4%

Total top 10 60.40 60%

Saudi Arabia 3.08 3%

World

Brazil

total 100.37

3.06 3%

South Korea 2.57 3%

1 Oil includes crude oil, all other petroleum liquids, and biofuels.

Canada 2.53 3%

2 Source: International Energy Statistics, Total oil (petroleum and other liquids) consumption, Decem

Germany 2.33 2%

Total top 10

2020. 60.40 60%

World total 100.37

Learn more:

1 Oil includes crude oil, all other petroleum liquids, and biofuels.

Energy

2

Explained: Where our oil comes from

Source: International Energy Statistics, Total oil (petroleum and other liquids) consumption, Decembe

2020.

Last updated: April 1, 2021

Learn more:

Energy Explained: Where our oil comes from

Other FAQs about Oil/PetroleumVous pouvez aussi lire