President Biden pledges an ambitious climate strategy

←

→

Transcription du contenu de la page

Si votre navigateur ne rend pas la page correctement, lisez s'il vous plaît le contenu de la page ci-dessous

President Biden pledges an ambitious climate strategy By Patrick Lenain, OECD Economics Department Ten years ago, the OECD published an in-depth analysis of U.S. greenhouse gas emissions (GHG) and urged the country to reverse gears (Carey, 2010). The analysis welcomed President Obama’s pledge in Copenhagen to cut the country’s emissions by 17% in 2020 from 2005 levels, but found that this would require new policy measures. As we approach the new climate summit in Glasgow (COP26), the United States can display progress: according to the latest data released by the Environment Protection Agency, GHG emissions have declined and President Obama’s target is within reach (Figure 1). President Biden has now pledged further progress with a target to cut GHG emissions by at least half in 2030 and achieve zero net emissions no later than 2050. These targets will imply to bend the curve and accelerate the pace of emission cuts. Figure 1: A faster pace of emission reductions is required Note: When published, 2020 data will show a sharp decline of

emissions caused by the COVID19 recession, but emissions are

likely to rebound in 2021 with the recovery of activity.

Source: Environmental Protection Agency.

The United States has already achieved a welcome reduction in

GHG emissions. At first glance, this seems surprising after

policy changes made during the Trump Administration such as

the repeal of the Clean Air Act, subsidies favouring fossil

fuels, and curbs on state-level regulatory standards. The

reasons for this progress is that a lot has happened in the

energy market, at the subnational level, and with tax credits:

Electricity production has been gradually decarbonised

thanks to the decline of coal, the rise of natural gas,

and the emergence of renewable energy sources such as

wind turbines and photovoltaic panels (Figure 2), which

have been encouraged by subsidies and regulation.

Cap-and-trade carbon markets have encouraged this energy

transformation at the regional level. The Regional

Greenhouse Gas Initiative (RGGI) is an agreement between

nine states that aim at curbing CO 2 emissions in the

electric power sector. RGGI helped to reduce emissions

in 2020 by 47% relative to 2005 in these states.

California and Quebec have also joined forces and

maintain a multi-sector cap-and-trade market.

Several tax credits already encourage households, firms,

and utilities to use clean energy and improve their

energy efficiency: an investment tax credit partially

pays for the cost of installing photovoltaic solar

panels; a plug-in electric vehicle tax credit helps

buyers of new electric vehicles; a producer tax credit

subsidizes the use of renewable energy sources.

Many other policy interventions seek to curb emissions

at the federal level (e.g. financial support to research

in renewable energy), state level (e.g. California’s

vehicle emission rules) and city level (e.g. Seattle’s

ban of combustion engine cars by 2030). In addition,

many U.S. firms have made net zero emission pledges, and

financial institutions have plans to withdraw funding to

the fossil fuel industry.

Figure 2: Coal is no longer favoured in electricity production

Source: OurWorldinData based on BP and Ember.

Despite past progress, much remains to be done in the United

States, like in many other countries, to limit the rise in

global temperature. The United States still emits the largest

amounts of GHG and CO2 per capita among G20 countries, together

with Australia and Canada. The effective pricing of energy-

related carbon emissions in the United States is among the

lowest in G20 and OECD countries: only 22% of these emissions

are priced at €60 per ton of CO2 or more, the level considered

as the minimum to reach the Paris climate targets (OECD,

2021a).

High energy prices are often favoured in terms of cost

efficiency, but they would have a regressive impact on income

distribution and are politically challenging. President Biden

has therefore announced alternative measures to lower GHG

emissions:

Tax credits will be further increased to decarbonise

electricity production and encourage energy efficiency.

Such tax credits can act like carbon taxes because they

reduce the cost of renewable energy relative to fossil

fuels. However, their impact is limited to specific

sectors, unlike economy-wide carbon taxes, and their

fiscal impact is negative because they reduce government

tax revenue.

The purchase of plug-in electric cars will be encouraged

by tax credits and public investment in battery

recharging stations. Ownership of electric vehicles in

the United States is one of the lowest in the OECD and

G20 and the Administration plans to catch up with other

countries.

More public investment will help the green transition.

Investment will strengthen the nation’s electricity

grid, and financial support will target the energy

efficiency of buildings.

President Biden’s plans are a big step forward toward a low

carbon future. The measures will help to decarbonise

electricity generation and transportation, but questions

remain about other large emitting sectors, especially industry

and agriculture (Figure 3).

Figure 3: Transportation and electricity sectors are large GHG

emitters, 2019

Source: Environmental Protection Agency. References: Carey, D. (2010), “Implementing Cost-Effective Policies in the United States to Mitigate Climate Change”, OECD Economics Department Working Papers, No. 807, OECD Publishing, Paris, https://doi.org/10.1787/5km5zrs4kc6l-en. OECD (2021a), Effective Carbon Rates, Pricing Carbon Emissions through Taxes and Emissions Trading. OECD (2021b, forthcoming), Assessing the economic impacts of environmental policies – Evidence from a decade of OECD research, OECD Publishing. Une occasion unique de bâtir

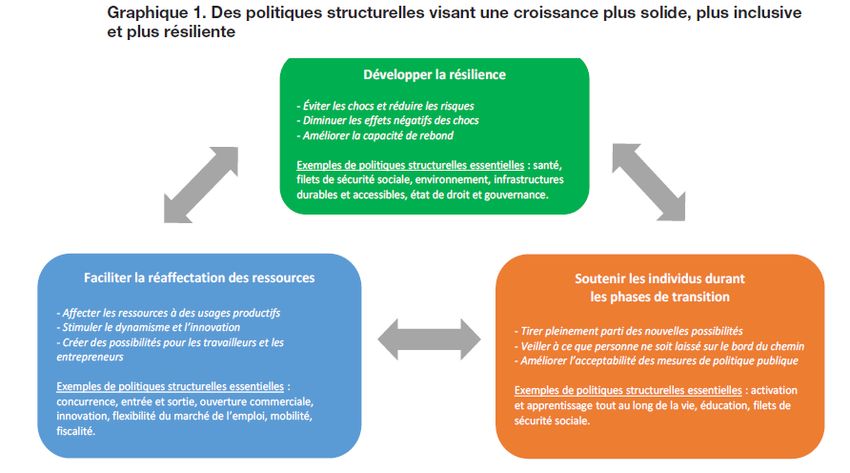

une reprise dynamique par Laurence Boone Cheffe économiste de l’OCDE et Représentante de l’OCDE au G20 pour les affaires financières Après une année 2020 dévastatrice, les perspectives s’éclaircissent. La dynamique vaccinale nous donne de l’espoir tandis que les mesures monétaires et budgétaires exceptionnelles continuent de soutenir les entreprises, les emplois et les revenus, limitant les retombées sociales et économiques de la pandémie. Fait important, la crise liée au COVID-19 a mis en évidence les mécanismes par lesquels les faiblesses structurelles peuvent saper la résilience de nos économies. Les mesures que nous prenons seront déterminantes pour la reprise et l’avenir de nos économies. Les gouvernements doivent agir dès à présent pour lever les obstacles structurels à la croissance; développer la résilience et la durabilité; stimuler la productivité et faciliter la réaffectation des ressources; et aider les individus à s’adapter au changement. Le coût de l’impréparation à la crise du COVID-19 s’est soldé par des pertes en vies humaines, une dégradation des moyens de subsistance et des séquelles sociales et économiques durables. La plupart des systèmes de santé ont dû affronter une vague épidémique mondiale d’une ampleur inédite. Selon les économies, les filets de protection sociale étaient plus ou moins prêts à faire face aux conséquences des périodes de confinement. Les pertes d’emplois et de revenus qui ont suivi ont souvent touché le plus durement les individus les plus

vulnérables. De larges pans de l’activité économique, sociale et éducative ayant basculé en ligne, les coûts d’opportunité des compétences numériques limitées et des infrastructures insuffisantes se sont matérialisés. Pour amortir le choc, les gouvernements ont réagi en prenant des mesures d’urgence d’une taille et d’une ampleur inédites. Pourtant, ces mesures ne règleront pas les problèmes structurels sous-jacents qui sont en fait à l’origine de notre vulnérabilité. La crise n’a fait que s’ajouter aux difficultés préexistantes. Avant la pandémie, nombre d’économies étaient confrontées à une faible croissance de la productivité dans un contexte de dynamique des entreprises en déclin. Le chômage de longue durée, l’économie informelle ainsi que la qualité et la sécurité médiocres des emplois étaient autant de problèmes caractérisant beaucoup de marchés du travail. De plus, la durabilité environnementale et les préoccupations plus générales relatives à la résilience étaient souvent absentes des stratégies en faveur de la croissance. Avec la réouverture des économies dans un monde défini par une montée en puissance du numérique, une évolution des environnements de travail, des restructurations d’entreprise et une transformation de l’emploi, les réformes visant à améliorer la dynamique des affaires et la croissance de la productivité doivent également aider les individus et les entreprises à s’adapter et à réaffecter leurs ressources afin de saisir les nouvelles chances qui s’offrent à eux. La publication Objectif croissance 2021 contient des conseils de première main à l’intention des gouvernements des économies de l’OCDE et des grandes économies non membres concernant les priorités des politiques structurelles à mener pour parvenir à une reprise dynamique. Elle constitue la contribution de l’OCDE au débat portant sur les mesures que les gouvernements doivent prendre pour rompre avec les pratiques non viables du passé et faire advenir une croissance plus forte, plus résiliente, plus équitable et plus durable.

La pandémie a également mis en évidence l’importance de la coopération internationale, gage d’une action publique plus efficace et moins coûteuse. C’est la raison pour laquelle nous mettons en avant, pour la première fois, les priorités de la coopération internationale dans les domaines de la santé, du changement climatique, des échanges internationaux et de la fiscalité des entreprises multinationales. C’est seulement ensemble que nous irons plus loin. A lire: Objectif Croissance 2021: Pour une reprise dynamique Un’opportunità unica per dare forma a una ripresa vigorosa

Laurence Boone OECD Chief Economist and G20 Finance Deputy Dopo un 2020 devastante le prospettive stanno migliorando. Il lancio dei vaccini infonde speranza, mentre straordinari dispositivi fiscali e finanziari continuano a sostenere le imprese, i posti di lavoro e i redditi, limitando le ripercussioni sociali ed economiche della pandemia. È importante notare che il COVID-19 ha evidenziato come le debolezze strutturali possano pesare sulla resilienza economica. Il modo in cui risponderemo condizionerà la ripresa e il futuro delle nostre economie. I governi devono agire ora per affrontare gli ostacoli strutturali alla crescita, costruire la resilienza e la sostenibilità; stimolare la produttività e facilitare la riallocazione; e aiutare le persone ad adattarsi al cambiamento. Il costo della mancata preparazione al COVID-19 si conta in vite umane, perdita di mezzi di sussistenza e cicatrici sociali ed economiche a lungo termine. La maggior parte dei sistemi sanitari ha lottato contro un’epidemia globale di una portata senza precedenti. Le reti di sicurezza sociale non erano tutte ugualmente preparate per affrontare le conseguenze dei lockdown. Sono stati persi posti di lavoro e redditi, e le persone più vulnerabili sono state spesso le più colpite. Se da un lato gran parte dell’attività economica, sociale ed educativa veniva effettuata online, dall’altro i costi in termini di opportunità dovuti alle scarse competenze digitali e all’insufficienza delle infrastrutture si sono fatti evidenti. I governi hanno reagito adottando misure di emergenza, senza precedenti per dimensioni e portata, per

mitigare gli effetti della crisi innescata dalla pandemia. Ma tali misure non permetteranno di risolvere i problemi strutturali sottostanti che ci hanno reso vulnerabili. La crisi non ha fatto altro che accentuare i problemi già esistenti. Prima della pandemia, molte economie lottavano contro una crescita lenta della produttività in un contesto di declino delle dinamiche aziendali. I problemi strutturali in molti mercati del lavoro includevano una disoccupazione a lungo termine ostinatamente alta, l’informalità e la scarsa qualità e sicurezza del lavoro. Inoltre, la sostenibilità ambientale insieme a preoccupazioni più generali di resilienza erano spesso assenti dalle strategie di crescita. In un momento in cui le economie si rimettono in moto in un mondo caratterizzato da una crescente digitalizzazione, cambiamenti nelle pratiche di lavoro, ristrutturazione aziendale e trasformazione dei posti di lavoro, le riforme per migliorare il dinamismo delle imprese e la crescita della produttività devono anche aiutare le persone e le imprese ad adattarsi e a riqualificarsi per cogliere le nuove opportunità. Going for Growth 2021 fornisce indicazioni concrete ai governi dei Paesi dell’OCSE e delle principali economie non OCSE sulle priorità di politica strutturale necessarie per favorire una ripresa vigorosa. Rappresenta il contributo dell’OCSE al dibattito sulle azioni che i governi devono intraprendere per non perpetuare le pratiche insostenibili del passato e raggiungere una crescita più forte, più resiliente, più equa e sostenibile.

La pandemia ha anche sottolineato quanto sia importante la cooperazione internazionale affinché l’azione politica sia più efficace e meno costosa. Ecco perché, per la prima volta, stiamo proponendo alcune priorità per la cooperazione politica internazionale in termini di assistenza sanitaria, cambiamento climatico, commercio globale e sulla tassazione delle imprese multinazionali. Agendo insieme potremo raggiungere risultati più grandi. >> Panorama economico sull’Italia >> Going for Growth: Shaping a vibrant recovery Going for Growth: Shaping a vibrant recovery

by Laurence Boone, OECD Chief Economist and G20 Finance Deputy A unique opportunity to shape a vibrant recovery After a devastating 2020, prospects are improving. The rollout of vaccines is giving us hope while extraordinary monetary and fiscal buffers continue to support firms, jobs and incomes, limiting the social and economic fallout of the pandemic. Importantly, COVID-19 has exposed how structural weaknesses can weigh on economic resilience. How we respond will shape the recovery and the future of our economies. Governments need to act now to address the structural obstacles to growth, build resilience and sustainability; boost productivity and facilitate reallocation; and help people adapt to change. The cost of unpreparedness to COVID-19 is counted in lives lost, livelihoods damaged and in long-lasting social and economic scars. Most healthcare systems struggled with a global outbreak on such an unprecedented scale. Social safety nets were unevenly prepared for dealing with the consequences of lockdowns. Jobs and incomes were lost with the most vulnerable people often the hardest hit. As large parts of economic, social and educational activity moved on-line, the opportunity costs of limited digital skills and insufficient infrastructure became real. Governments reacted with emergency measures, unprecedented in size and scope, to cushion the shock. Yet the measures will not fix the underlying structural problems, which left us vulnerable in the first place.

The crisis has only added to pre-existing challenges. Before the pandemic, many economies were struggling with sluggish productivity growth amid declining business dynamics. Structural problems in many labour markets included stubbornly high long-term unemployment, informality and poor job quality and security. Moreover, environmental sustainability alongside more general resilience concerns were often absent from growth strategies. As economies reopen in a world of rising digitalisation, changes to workplace practices, corporate restructuring and job transformation, reforms to enhance business dynamism and productivity growth also need to help people and firms adjust and reallocate in order to seize new opportunities. Going for Growth 2021 provides first-hand advice to governments of OECD and major non-OECD economies on the structural policy priorities needed for a vibrant recovery. It is the OECD’s contribution to the debate on what governments need to do to break away from unsustainable past practices and achieve stronger, more resilient, more equitable and sustainable growth. The pandemic has also underlined the importance of

international cooperation, which can make policy action more effective and less costly. This is why, for the first time, we are putting forward priorities for international policy cooperation: in healthcare, on climate change, on global trade and on the taxation of multinational enterprises. By acting together can help to achieve more. Laurence Boone OECD Chief Economist and G20 Finance Deputy Further reading: OECD (2021), Economic Policy Reforms 2021: Going for Growth, OECD Publishing, Paris, https://doi.org/10.1787/3c796721-en. American Rescue Plan: A first package of President Biden’s transformative reforms By Patrick Lenain, Carl Romer and Ben Westmore The American Rescue Plan (ARP) submitted by President Biden and approved by U.S. Congress in mid-March provides US$1.84 trillion (8.4% of GDP) of fiscal support to the economy — a very large stimulus by international standards. Soon after the

plan’s approval, the OECD Interim Economic Outlook presented a significant upward revision to the U.S. economic growth forecast, doubling it for 2021 from 3.2% to 6.5%. The fiscal package will boost domestic demand and help activity return more quickly to pre-pandemic levels (Figure 1), with many unemployed workers getting back jobs. Furthermore, OECD modelling highlights that the package may have noteworthy demand spillovers for the major trading partners of the U.S. (for further details, see The American Rescue Plan is set to boost global growth). Figure 1: U.S. GDP projections (trillion of US dollars, constant prices) Source: OECD Economic Outlook projections. While concerns have been raised that such a large fiscal stimulus could cause a significant future inflation shock, the transformative content of the measures in the package should not be overlooked. As recommended by successive OECD Economic Surveys of the United States, the ARP seeks to address persistent structural challenges that have prevented many Americans from realising their human potential. The Plan will help struggling subnational governments, support unemployed workers, facilitate the reopening of schools, close gaps in unemployment insurance, and reduce child poverty. Besides sending checks of $1400 to eligible families (budget cost of US$412 billion), the Plan contains other important provisions

(Figure 2).

Figure 2 – American Rescue Plan’s main provisions*

Source: Authors’ compilation from various sources.*

Estimates based on available information and subject to

changes.

Support to subnational governments (US$350 billion). The

ARP allocates financial support to States, territories

and tribes. States that depend on tourism and sales

taxes like Hawaii, Nevada, Florida, Texas have faced

steeper budget shortfalls, whereas other states like

Idaho and Utah saw large revenue increases owing to

strong federal expenditures and relatively short

COVID-19 lockdowns. As argued in past OECD work,

subnational governments play key social and economic

roles, but existing fiscal rules can impose damaging

spending cuts during recessions.

Unemployment relief (US$246 billion). The Plan provides

Federal funding to supplement state-level unemploymentinsurance benefits with an additional $300 per week – less than the supplement of $600 per week in the CARES Act but nonetheless important, as these benefits would otherwise have fallen back to low pre-crisis levels. By supporting unemployment insurance, the ARP will help to keep unemployed workers active in the labour market, rather than becoming discouraged from job search, as seen in past recessions. Support to schools and higher education (US$170 billion). Manyschools had to close during shutdown orders, with detrimental impacts on vulnerable families and the risk of large numbers of dropouts. K-12 Schools will be given US$125 billion in direct aid with another US$40 billion for colleges and universities to reopen in safe conditions. Reducing gaps in educational outcomes, as measured by PISA, has been a recurring OECD policy recommendation. Child benefits and affordable childcare (US$156 billion). A persistent challenge for families has been the absence of affordable childcare, which has depressed the labor-market participation of American women. Also, the lack of affordable early-childhood education, which is decisive in children’s school performance, has created large inequalities. The ARP provides emergency funding for child-care assistance to essential workers unable to telework, typically people in low-income deciles. The Plan also helps 16 million poor and rural K-12 students without access to high-speed internet. The Child Tax Credit and Earned Income Tax Credit will receive a much-needed boost: the Urban Institute projects that this will cut child poverty in half. Health insurance coverage, vaccines and COVID-19 containment (US$125 billion). PastOECD work has recommended closing existing gaps in healthcare insurance, working towards universal coverage through a system of multiple insurance providers. For employees laid off or who otherwise lost their health insurance,

ARP provides US$57 billion in funding for employers to

retain COBRA coverage for departing employees and a

temporary expansion in subsidies that could be used to

pay for health coverage through the Affordable Care Act

public exchange system. In addition, ARP increases

marketplace premium subsidies for people at every income

level and will now be offered to those with income above

4 times the federal poverty level.

While these measures are temporary, the OECD has recommended

permanent reforms to alleviate child poverty, improve K-12

education, close gaps in health insurance, and strengthen

local communities – all with a beneficial impact on long-term

economic growth and well-being. Other reforms recommended by

the OECD include wider access to high-speed internet;

investment in green technologies; and strengthening anti-trust

actions to protect consumers against oligopolies’ market

dominance.

President Biden has now turned his attention to implementing

new policies to boost investment, which could have a fiscal

cost of at least US$3 trillion spread across several years.

Notwithstanding the risk of political gridlock, this provides

the opportunity to further address long standing challenges,

including those reform priorities previously identified by the

OECD in the areas of infrastructure, green technologies and

education.

References

OECD (2021), “The need for speed: Putting the World Economy on

the Fast Track out of the COVID-19 crisis”, ECOSCOPE blog, 17

March.

OECD (2020), Economic Survey of the United States, OECD

Publishing, https://doi.org/10.1787/12323be9-en

Azzopardi, D., F. Fareed, M. Hermansen, P. Lenain and D.

Sutherland (2020), “The decline in labour mobility in theUnited States: Insights from new administrative data Azzopardi, D., F. Fareed, M. Hermansen, P. Lenain and D. Sutherland (2020), “Why are some U.S. cities successful, while others are not? Empirical evidence from machine learning”, OECD Economics Department Working Paper No. 1643. Indonesia: making the economic recovery sustainable and inclusive by Andrea Goldstein, OECD Economics Department Despite the recession, the first in 20 years, Indonesia avoided an even larger downturn in 2020 thanks to a credible economic policy response. The latest OECD Economic Survey of Indonesia acknowledges that the size of the support was constrained by low tax revenue and underscores that disbursing the package proved initially difficult and slow. But it was accompanied by economic reforms, showing that meaningful efforts at improving market functioning can be made even in the midst of a severe crisis.

The economy is recovering. GDP shrunk by 2.1% in 2020 and

the Survey sees growth of 4.9% for 2021 and 5.4% in 2022. The

rebound is sustained by pent-up demand for consumer goods and

capital goods and will gain momentum as containment measures

are phased out and vaccination progresses to the entire

archipelago of 17 000 islands.

1. Other G20 EMEs include Argentina, Brazil, China, India,

Mexico, Russia, Saudi Arabia, South Africa, and Turkey.

Source: OECD Economic Outlook 108 database updated.

The economic outlook is surrounded by substantial risks and

uncertainties

Most Indonesians work in the informal sector and their

limited savings were used to guarantee basic necessities

during lockdowns. The emerging middle class that was

celebrated in the 2010s found itself much more

vulnerable than expected – how fast will it regainconfidence and therefore access finance to resume

spending, especially in consumer durables?

On the upside, the global recovery could be stronger

than expected and boost demand for Indonesian goods and

services.

On the downside, Indonesia, which will chair the G20 in

2022, is subject to the same investors’ fickleness as

other emerging markets and may suffer from contagion

effects if a peer, no matter how distant and different,

falls into crisis. An additional risk is that

international travellers may stay away from far-flung

destinations where medical services are deemed poor.

While the economy is fragile, macroeconomic support is needed

The independent central bank should maintain its

accommodative stance, geared towards supporting the

recovery, while providing forward guidance regarding

normalisation of monetary conditions.

With so many households and firms suffering from the

crisis and the risk of long-lasting scarring effects, it

is sensible to maintain fiscal support to the economy.

Additional efforts can be made to ensure that resources

are directed at those most in need. Tax policy reforms

should continue, to fight against evasion and erosion

and make the system fairer with more people paying their

due.

Structural reforms can contribute to make the recovery

stronger, fairer and greener

Firms and households flourish and make forward-looking

decisions when governments provide the right conditions to

take calculated risks and policies are predictable and

consistent.

Indonesia is still characterised by a high number of

restrictions that benefit selected and well-connectedgroups. This is true for labour market rules that protect employees and not jobs, as well as for product market regulations that make it difficult for new entrants to challenge incumbents. But where conditions are right, the results are impressive. Establishing a start-up is rather easy and affordable: it is no coincidence that Indonesia can boast five unicorns (i.e. high-tech firms valued USD 1 billion and more) versus three in Australia and four in Japan. The Omnibus Bill on Job Creation, approved in late 2020, includes a large number of changes that will hopefully make it easier for domestic and foreign firms to operate and invest in Indonesia. And it will be fundamental that they do so in full respect of the rules of the game and of international best standards. This translates into respect for labour and environmental rights and determination in upholding business integrity. The government and parliament should play their part too: the post-pandemic period, for instance, will see many

public works adjudicated, and there is no need to prefer

direct awards over the transparency of open tenders.

The crisis has not been neutral. Informal workers who are not

covered by social security, women who are either housewives or

both work and take care of the family, people with

disabilities, youngsters and migrants – these groups have

suffered disproportionally from the crisis. But so did

children who missed a good part of the school year, at least

in terms of in-person education, and will suffer the

consequences for the rest of their life. These developments

add to pre-existing challenges in providing relevant and

adequate skills to a population that remains young but will

soon reach the peak of the demographic dividend.

These issues are covered in the Survey’s in-depth chapter on

education and skills. There is no easy answer, but a

combination of measures that would help. Early childhood

education, for instance, has a lasting effect on educational

performance, at the same time as it makes it easier for women

to combine work and maternity. Vocational education and

training should also be reinforced, removing any stigma it has

compared to standard education. And foreign investment in

tertiary education, as contemplated by the new economic

cooperation agreement with Australia, would improve the

quality of Indonesian universities.

Reference:

OECD (2021), OECD Economic Surveys: Indonesia 2021, OECD

Publishing, Paris – OECD.KappaThe American Rescue Plan is set to boost global growth by Nigel Pain and Patrice Ollivaud, OECD Economics Department Global economic prospects have improved markedly in recent months, helped by the gradual deployment of effective vaccines against Covid-19, announcements of additional policy support in several countries, and signs that economies are coping better with measures to supress the virus. This is reflected in the stronger recovery shown in the new OECD Interim Economic Outlook, with global GDP growth now projected to be 5½ per cent in 2021 and 4% in 2022. Strong and timely fiscal support since the onset of the pandemic has played a vital role in supporting incomes and preserving jobs and businesses. This should be maintained whilst economies are still fragile and growth remains hampered by containment measures and incomplete vaccination deployment. As economies reopen, new discretionary fiscal measures can also be an effective means of helping to close the large shortfalls of output and jobs from their normal, pre-pandemic levels. The substantial fiscal support being provided in the United

States this year is an important factor behind the improved global outlook. Already, the package of measures enacted in December 2020, worth USD 900 billion (4% of GDP), has boosted household incomes and, to a smaller extent, consumer spending at the start of 2021. The new American Rescue Plan of USD 1.9 trillion (8½ per cent of baseline GDP) provides a considerably larger additional stimulus that should raise aggregate demand substantially in the United States, with welcome spillovers for activity around the world. There is likely to be a clear immediate boost from stimulus payments to households, which represent around one-fifth of the overall package of measures. Other measures in the Plan are only partly pandemic-related and will take effect over the next year or so. Futher details on the content of the American Rescue Plan will be provided in a future blogpost. Illustrative simulations on the NiGEM global macroeconomic model suggest that the measures in the American Rescue Plan could raise US output by around 3-4 per cent on average in the first full year of the package (from 2021Q2 to 2022Q1). This is broadly equivalent to the spare capacity estimated to exist in the US economy in the December 2020 OECD Economic Outlook. The US upturn also helps to stimulate demand in all other economies. Output is raised by between ½‑1 percentage point in Canada and Mexico, both close trading partners of the United States, and between ¼‑½ percentage point in the euro area, Japan and China (see Figure). Overall, global GDP is boosted by around 1% during this period.

In these simulations, stronger US domestic demand improves near-term job prospects, with US employment rising by between 2¼‑3 million by the end of 2021 and the unemployment rate declining by between 1¼-2 percentage points. The demand upturn also boosts import growth and widens the US current account deficit by around ¾ per cent of GDP on average in the first four quarters of the shock, despite higher US exports due to stronger foreign demand. US price inflation picks up temporarily, by around ¾ percentage point per annum on average in the first two years of the shock, but not to a rate that would necessarily require any immediate policy tightening by the Federal Reserve given the new US monetary policy framework. The overall budgetary cost in the near term is lower than the size of the stimulus, with higher nominal activity offsetting around one-quarter of the cost of the discretionary stimulus measures. Even so, the US general government debt-to-GDP ratio is raised by 6 percentage points by 2023. These simulations show the impact of an illustrative mix of higher transfers to households, stronger final government consumption and tax reductions introduced over 2021Q2-2022Q2. The near-term impact of the US fiscal package will be relatively large if consumers are “backward-looking” and more sensitive to current income developments and the impact of

higher government transfer payments. In contrast, “forward- looking” consumers, more focused on the lifetime income path of incomes and the potential budgetary offset from higher tax payments in the future, may spend less of the stimulus, resulting in smaller spillovers to other countries. In either case, there are substantial near-term gains to output and the risks of lasting damage from a slow recovery have been reduced considerably. Further ahead, the direct impact of the Plan on output and inflation may be modest, reflecting the temporary nature of the fiscal stimulus, although there could be a lasting boost to the size of the labour force from attracting back previously discouraged workers. Growth prospects would also be improved if innovation and investment were raised permanently (relative to baseline). A faster recovery from the pandemic and additional policy measures to help foster investment would raise the chances of such an outcome. See also The need for speed: Putting the World Economy on the Fast Track out of the COVID-19 crisis Reference: OECD (2021), OECD Economic Outlook, Interim Report March 2021, OECD Publishing, Paris, https://doi.org/10.1787/34bfd999-en. The need for speed: Putting the World Economy on the Fast

Track out of the COVID-19 crisis by Laurence Boone, OECD Chief Economist This is no ordinary economic crisis. When you walk down the street of a big city like Paris, its hard not to miss the usually lively restaurants, bars and museums. Travel and activity restrictions – completely unfamiliar to most of us just one year ago, have now become a part of our daily lives. In early March 2020, the OECD warned that COVID-19 could have devasting effects on the world economy. One year later, amid high uncertainty, a global recovery is in sight. We have upgraded our growth projections The good news is that the world economy is doing better than what we expected only three months ago. Countries are learning to better address the health situation, some are rolling out vaccines and are gradually lifting restrictions to mobility. People and firms have also adapted: producing, trading and consuming differently in this new world of restrictions. Undeniably, policy support helps. The exceptional fiscal and monetary support that countries have deployed to protect firms

and people is working – supporting jobs, incomes and firms. In addition, the massive foreseen US stimulus (USD 1.9 trillion in addition to USD 900 billion in December 2020) will boost the US economy in 2021 and add a full percent to world output in our projection as discussed in our recent post on the American rescue plan. As a result, we project global growth of 5.6% in 2021 (Table 1), up from 4.2% in our December projections. Most countries are bouncing back, but activity levels remain far behind where we expected them to be in our November 2019 projections before the pandemic. Moreover, divergence in economic performance across and within countries is set to increase. The best economic policy to exit this global pandemic is rapid vaccination, worldwide Differences in health management and vaccine rollout, and consequently restrictions, as well as sectoral specialisation in hard-hit sectors such as tourism and policy support are driving the increase in divergence. Several emerging market economies, as well as European ones, are lagging behind in the recovery (Figure 1).

To speed up the rollout of vaccines, policymakers need to get on a wartime footing with vaccine production and distribution. Production is currently being scaled up thanks to voluntary licensing, but more can be done. Governments should encourage the maximum use of existing manufacturing vaccine facilities and distribution networks, while fast-tracking consents for new facilities where necessary. This means using government purchasing leverage to foster private sector licensing, transfer of technology deals and a cooperative effort across firms that would normally be competitors. Regarding the distribution of vaccines, this means governments requiring and funding vaccination centres to operate seven days per week and long hours. To be effective, vaccine rollout needs to be not only fast, but also global. This is the only way to win the race against virus mutations and to fully reopen sectors such as travel and tourism, which accounts for over 20% of GDP in some countries. As long as the virus is raging somewhere, the risk of new virus variants is high, which will mean that we will need to keep some borders shut, restraining activity. A coordinated and multilateral approach to licensing and technology

transfers, as well as purchasing, notably through increasing funding to COVAX, is the most efficient way of scaling up production and distribution worldwide, and especially in emerging markets. Fiscal support has been key in preserving the economic and social fabric Widespread vaccination will also make fiscal and monetary support more effective. The countries that are able to combine fast vaccination with supportive macroeconomic policies are the ones expected to benefit from faster recoveries (Figure 2). As our economies re-open, many entertainment hotel and restaurant workers can hope to get back to work. But, prospects are not the same for everyone. Following the Global Financial Crisis, young people struggled to find employment and policy was too slow to react – it took a decade for the employment prospects of graduates to “normalise” (Figure 3). To avoid such a negative outcome and the scarring effects of unemployment this time around, fiscal policy needs to be better targeted at supporting young people, for example by introducing wage subsidies to help firms expand apprenticeship and in-firm training programmes. It also needs to make use of the opportuntity to pave the way forward for a better future – fixing the massive digital divide exposed by the pandemic and directing investment to support environmental sustainability.

With the arrival of vaccines, the world economy will eventually fully re-open for business. But how the recovery is going to shape up is in the hands of policymakers: swift

vaccination, targeted fiscal support and ramping up investment

in new and green technologies can make a difference. Many

challenges lie ahead but this crisis has taught us the

importance of resilience: our ability to both avoid and

respond to shocks. And, without multilateral co-operation the

global recovery in growth and the jobs that go with it are at

risk. There is no time to waste!

Reference:

OECD (2021), OECD Economic Outlook, Interim Report March 2021,

OECD Publishing, Paris, https://doi.org/10.1787/34bfd999-en.

Technology, Labour Market

Institutions and Early

Retirement: Evidence From

Finland

Ɨ

by Naomitsu Yashiro*, Tomi Kyyrä , Hyunjeong Hwang* and Juha

ǂ

Tuomala@ Shutterstock/ SpeedKingz Across OECD countries, promoting longer working lives is an important policy agenda for mitigating fiscal pressures from increasing pension and healthcare expenditures. There are, however, two significant barriers to increasing employment of older workers, especially in the context of digitalisation. First, workers engaged in codifiable, routine tasks are prone to being displaced by computers and robots (Gentile et al., 2020), a trend that may have been accelerated by the COVID-19 pandemic (Baldwin, 2020; Chernoff and Warman, 2021). Older workers are particularly exposed to this risk because, with shorter remaining working lives, they have weaker incentives to acquire new skills that would allow them to switch to tasks that are less likely to be automated. They may instead choose to retire early when facing rapid technological change (Ahituv and Zeira, 2011; Hægeland et al., 2007). Second, a number of OECD countries have in place institutions that encourage early retirement, such as exceptional entitlements for older workers or looser criteria for unemployment and disability benefits than for other workers. These two factors reinforce each other in pushing older workers out of employment: older workers who are more exposed to new technologies are more likely to exit the labour market when they have access to institutional

pathways to early retirement; and older workers who have

access to early retirement pathways are more likely to use

them when they are more exposed to technological change.

Our paper explores such complementarity for Finland, a country

renowned for its intensive use of digital technologies but

also with a considerably lower employment rate for older

individuals than in other Nordic countries (OECD, 2020). The

latter is driven importantly by early retirement through the

so-called unemployment tunnel, which is the combination of the

entitlement to unemployment benefit of up to 500 working days

and the extension of unemployment benefit until the retirement

age reserved for the unemployed aged 61 or over who have

exhausted their regular unemployment benefit entitlements.

From an empirical analysis exploiting a rich Finnish employee-

employer database and the OECD data capturing exposure to

digital technologies, we find that:

An individual aged 50 or above in occupations exposed to

a standard deviation higher than the average risk of

automation (computed by Nedelkoska and Quintini, 2018)

faces a 1.1 percentage point higher probability of

exiting employment every year, if he or she does not

have access to the unemployment tunnel.

This probability is 2.2 percentage points higher if the

individual has access to the tunnel.

Gaining access to the unemployment tunnel increases the

exit probability of an individual exposed to an average

level of automation risks by 1.8 percentage points.

The overall impact of higher automation risks and the

unemployment tunnel therefore amounts to 4 percentage

points, which implies an 80% increase in the probability

of exiting employment for individuals aged 57-58.

We obtain similar results when using other indicators to

capture the exposure to digital technologies, such as

intensity in routine tasks (Marcolin et al., 2016) or ICT

skills (Grundke et al., 2017). Using the estimatedcoefficients, we simulate the impact of reforms that tighten access to the unemployment tunnel. Figure 1 illustrates that such reforms extend substantially the working lives of older workers exposed to high automation risks, but have little effect on individuals exposed to low automation risks. This paper underscores the importance of labour market reforms that tighten access to institutionalised early retirement pathways in ensuring the inclusion of older workers in the future of work. While previous policy discussion often emphasised boosting lifelong learning opportunities, older workers will only have weak incentives to take up such opportunities if these early retirement pathways are left open. The recent decision by the Finnish government to abolish extended unemployment benefit by 2025 for persons born in 1965 or after is likely to encourage older workers relatively exposed to technological change to work longer and participate in upskilling opportunities. This, however, calls for targeted

measures to increase the employability of groups most affected by this reform, namely low- and middle-skilled male workers in occupations exposed to high automation risks, involving more routine tasks and less use of ICT skills. Highly tailored training programmes as well as effective schemes for identifying the training needs of these older workers and certifying their acquired skills are important for boosting their upskilling efforts (OECD, 2020; 2019). Policy makers should also step up measures for getting older workers displaced by new technologies back into employment. In the case of Finland, such measures may include strengthening the capacity of the employment service to provide these workers with more personalised counselling and better monitoring of their activation requirements (OECD, 2020), as well as enhancing the role of social partners in facilitating job transitions even before dismissals take place, as in Sweden (OECD, 2016). *OECD Economics Department / ƗVATT Institute for Economic Research and IZA Institute of Labour Economics / ǂVATT Institute for Economic Research Further reading Naomitsu Yashiro, Tomi Kyyrä, Hyunjeong Hwang, Juha Tuomala (2021) “Technology, labour market institutions, and early retirement” VoxEU.org, 12 March 2021. Yashiro N., Kyyrä, T., Hwang, H. and J. Tuamola (2021), “Technology, labour market institutions and early retirement: evidence from Finland”, OECD Economics Department Working Papers 1659. OECD (2020), OECD Economic Surveys: Finland 2020, OECD Publishing, Paris. OECD (2019), Working Better with Age, Ageing and Employment Policies, OECD Publishing, Paris.

Reference Ahituv, A. and J. Zeira (2011), “Technical progress and early retirement”, Economic Journal, 121, 171–193. Baldwin, R. (2020) “Covid, hysteresis, and the future of work” VoxEU.org, 29 May Chernoff, A. and C. Warman (2021) “Down and out: Pandemic- induced automation and labour market disparities of COVID-19” VoxEU.org, 2 February. Gentile, E., S. Miroudot, G. De Vries and K. M. Wacker (2020) “Robots replace routine tasks performed by workers” VoxEU.org, 8 October. Grundke, R. et al. (2017), “Skills and global value chains: a characterisation”, OECD Science, Technology and Industry Working Papers, 2017/05. Hægeland,T., D. Rønningen and K. Salvanes (2007), “Adapt or withdraw? Evidence on technological changes and early retirement using matched worker-firm data”, NHH Dept. of Economics Discussion Papers, No. 22/07. Marcolin, L., S. Miroudot and M. Squicciarini (2016), “The routine content of occupations: new cross-country measures based on PIAAC”, OECD Science, Technology and Industry Working Papers, 2016/02. Nedelkoska, L. and G. Quintini (2018), “Automation, skills use and training”, OECD Social, Employment and Migration Working Papers, No. 202. OECD (2020), OECD Economic Surveys: Finland 2020, OECD Publishing, Paris. OECD (2019), Working Better with Age, Ageing and Employment Policies, OECD Publishing, Paris.

OECD (2016), Back to Work: Finland: Improving the Re- employment Prospects of Displaced Workers, OECD Publishing, Paris. Canada: Ensuring sustainable economic recovery by Philip Hemmings, OECD Economics Department Canada’s economic support averted an even larger downturn in 2020. The latest OECD Economic Survey of Canada underscores that the economic policy response to the crisis has been rapid, entailing one of the biggest support packages of OECD countries. Even with this support, the economic activity fell by over 12% between Q4 2019 Q2 2020.

Economic recovery is in sight. Although the latest round of

containment measures has slowed the rebound in activity, the

easing of restrictions as vaccination progresses will see the

recovery gather momentum. Following a shrinkage in output of

5.4% in 2020, the Survey sees growth of 4.7% for 2021 and 4%

in 2022.

Substantial risks and uncertainties surround the economic

outlook:

Many households accumulated sizable savings during

lockdowns. How fast consumer confidence, and therefore

spending, will rebound is uncertain—implying risks to

the projection.

On the upside, the boost from US stimulus could be

larger than expected.

On the downside, high household and corporate debt

contributes to macro-financial vulnerabilities.

The economy still needs macroeconomic support while the

economy is fragile:

Monetary policy should continue to be geared towards

supporting the recovery.

The targeted fiscal support to people and businesses

should evolve as the recovery progresses to ensure

assistance focuses support policies for workers in hard-

hit sectors and youth and viable companies.

Fiscal policy needs to look ahead. After the pandemic

subsides, it will be necessary to stabilise public debt and

find ways to accommodate additional spending commitments.

Canada’s significant policy support also means the public debt

has increased substantially. Furthermore, the ageing-related

spending pressures present before the pandemic will continue.

There is need for a clear and transparent roadmap in fiscal

policy that ensures the public debt burden does not spiral out

of control.Structural reform is also needed to reach a stronger and

greener growth in the post-covid era. Businesses need

conditions that will help them adapt to the future:

Stronger incentives for business to become greener are

also needed to help drive decline in greenhouse gas

emissions—Canada has a long way to go to achieve its

goals. The report supports the recent federal government

proposals for substantial carbon-price increases,

announced as part of a strengthened climate plan. It

also suggests Canada could expand its use of

environmental taxes more generally, which are low

relative to other countries’.

The economy would benefit from lower barriers to inter-

provincial trade and better high-speed Internet

infrastructure.

Evidence points to a need to re-examine insolvency

procedures to ensure that viable companies running into

difficulty have an opportunity to recover.The crisis has exacerbated socio-economic inequalities. Job losses have been greatest in low-wage sectors that employ substantial numbers of young people and women. The crisis has also highlighted disadvantages among ethnic minorities and Indigenous groups, who tend to fare poorly in terms of income, life expectancy, housing and health, even in normal times. It has also exposed shortcomings in areas like long-term care for the elderly, health policy and the provision of affordable housing. The recovery should be used to address these vulnerabilities. These issues are covered in the Survey’s in- depth chapter on well-being. Reference: OECD (2021), OECD Economic Surveys: Canada 2021, OECD Publishing, Paris, OECD Economic Surveys: Canada 2021 – OECD.Kappa https://doi.org/10.1787/16e4abc0-en

Vous pouvez aussi lire