Railway station financing mechanisms : international benchmarks - Proceedings Breakfast Discussion Tuesday, March 12, 2013

←

→

Transcription du contenu de la page

Si votre navigateur ne rend pas la page correctement, lisez s'il vous plaît le contenu de la page ci-dessous

Proceedings

Breakfast

Discussion

Tuesday,

March

12,

2013

Railway station financing

mechanisms : international benchmarks

Contents Opening Erreur ! Signet non défini. Remi DORVAL 2 President of La Fabrique de la Cité (The City Factory) Erreur ! Signet non défini. Railway station financing mechanisms Erreur ! Signet non défini. Richard ABADIE 3 Global Infrastructure Leader chez PwC 3 Discussion 15

Opening (in french)

Remi DORVAL

President of La Fabrique de la Cité (The City Factory)

Nous poursuivons aujourd’hui notre cycle sur le financement des infrastructures. Nous nous

étions réunis autour de l’étude menée avec l’OCDE sur le financement de la « croissance verte ».

Nous nous intéressons aujourd’hui au financement des gares. La Fabrique de la Cité ayant pour

principe d’apporter un éclairage international sur les grands problèmes de la ville, nous avons

demandé au cabinet PwC d’analyser les mécanismes financiers de quelques gares récemment

construites ou réhabilitées aux États-Unis, en Europe ou à Hong Kong. Il en ressort une grande

diversité dans les approches des différents pays, mais nous pouvons sans doute en tirer des idées

intéressantes.

Ce travail a mobilisé plusieurs personnes : Richard Abadie, qui a dirigé l’étude (PwC), Philippe

Bozier qui a coordonné l’étude avec l’aide de Clément Martin (PwC France), ainsi que Roberta

Odoardi et Francesco Gargani (PwC Italie).

2

Railway station financing mechanisms

Richard ABADIE

Global Infrastructure Leader, PwC

We will be talking about what we are seeing in the infrastructure market at the moment.

If we start with station development, it is quite important when we are looking at studies like this,

on railways mechanisms, not to just dive straight into the financing side. Probably like most of you, I

have travelled around the world quite a lot and I get to see and spend time in many, many railway

stations around the world. It is not always a very pleasant experience. Sometimes I would much

rather not be there. As I travel around the world, I ask myself, 'What is it that I like about railway

stations when I am in them?'

I have been to the railway station at Washington, DC. For those of you who have been through

there, you would remember it. It is an unbelievable station with incredible architecture. It is

something worth looking up on the Internet if you have time. For most of you who have not travelled

through the railway station in DC, I strongly recommend it. Many, many people visit that railway

station, not because they want to travel, but just to see the architecture and the like.

Now, the reason for highlighting some of those stations is just to show that at the end of the day,

with all those objectives in mind, a station has some aesthetic appeal. You want to go there. If you

want to turn it into a commercial enterprise, it must be somewhere you want to go into and possibly

remain, rather than just passing through as quickly as possible.

I have also travelled through Delhi station. I can tell you that the problem there is it is the type of

station you want to pass through very, very quickly. You do not want to spend time in Delhi station.

What you tend to find in Delhi station is that the economics of the station themselves are pretty

limited because people are not spending money when they go through there.

I have listed objectives in station development.

- The first one is that they are generally large assets and you want to showcase the

ability of the station. The second point is that as a traveller, you want to pass through

a station quite efficiently with limited impediments. As a user of any station in the

world, if you are going to spend your money in the station, a little bit like airports, you have

got to have retail facilities, commodities that are available to you at very, very short notice

and easy access.

- Then the other thing that we will get on to around financing is that there are very few

stations in the world that are commercially successful on a standalone basis that are not

attached to a wider urban development programme. We will go through some of the

case studies and I will show you what I mean by that.

Before I get onto that, I get asked very often, 'What is happening in the world of infrastructure

finance?' Now, this is partly relevant to station development, but probably the first point is the most

important one.

What we are seeing around the world, and it is no different in France, and the UK for that matter -

both countries have been downgraded recently - is that the traditional sources of capital for

infrastructure have been governments and cities borrowing money themselves and investing

it in infrastructure. That will still continue in future. Nothing will change in that regard. The

problem is that the cost of finance for governments and cities is going up as their credit ratings are

being downgraded.

3

The other thing we have seen, particularly in the Western world, are significant austerity

programmes where governments are looking to cut back spending rather than invest it. I draw a

parallel between the UK and France in this regard. France's infrastructure is much better than the

UK's, but the UK probably has a £250 billion infrastructure programme over the next 10 years. The

largest project in that infrastructure programme is what is called High Speed 2, the second high

speed line in the UK. That is going to cost £30 billion.

I understand that the “Grand Paris project” is about the same size in terms of €30 billion, £30

billion. These days, there is not much difference between the currencies. The point there is that it is

very difficult for governments alone to do this financing when they are of that size. For those of you

in the financing markets at the moment, it is very, very difficult to raise bank finance. Some of the

French banks I know are prepared to lend to some of the big sponsors, such as VINCI. They will do

that on a long-term project finance basis, but the level of debt in the markets is significantly down

because of regulatory pressures.

I mentioned many of the banks have exited the market while they try to delever. Many of the

banks that have left the market are either in trouble as banks - they have been nationalised - or

alternatively, they are trying to rebuild their capital basis and therefore lend less to projects.

The fourth point there is regarding governments around Europe, and I know in France,

there has been a review of the PPP model. I do not know where it has come out. I think François

Hollande has said that he will continue to support it, but that is happening again around the world.

There are reviews of the support structures that government have in place.

The last point, which is what I want to touch on because it is relevant to railway stations, is that

there is increased talk of capital markets, so that is project bonds, pension funds buying project

finance debt, insurance companies, institutional investors, infrastructure debt funds, guarantees and

the like. I will touch on that a little bit later. What I would say on this particular point, which is quite

interesting to me, is that the biggest new entrant into the infrastructure finance or project finance

4

market is Allianz. Allianz has set aside €1 billion to invest in greenfield infrastructure. I would expect

quite a lot of that to come to France and possibly to find its way into the railway station sector.

That is just a quick update, both on the objectives of stations and also some of the challenges

we are facing in the infrastructure finance market. It is important that we recognise stations in their

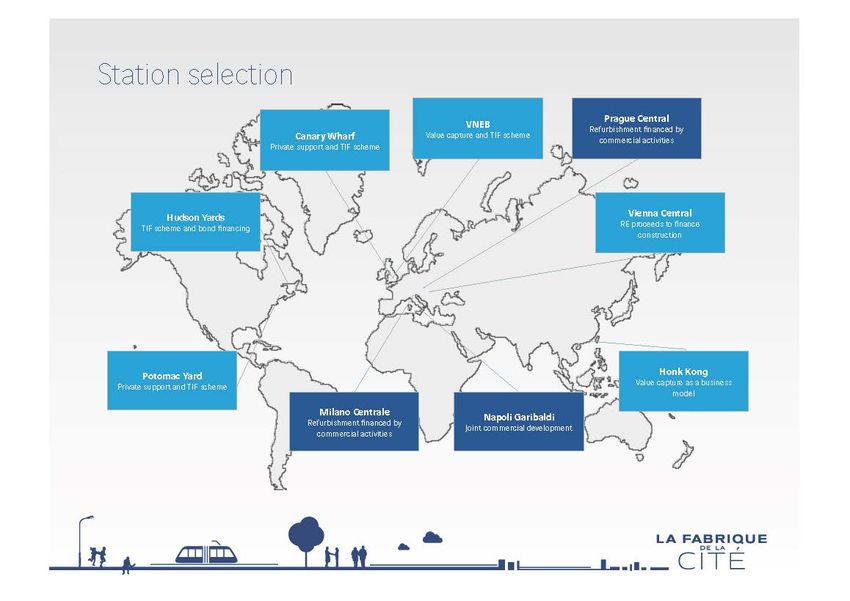

own right, rather than just as commercial enterprises. We looked at nine stations in our study. We

selected those stations in conversations with a couple of people in the market. These are by no

means the only stations that have used some source of innovative finance. I am sure if I went

around this room, there would be other examples as well, but there are nine examples.

I do not intend going through all nine of them today. You can go through them at your leisure.

All nine of those case studies are specifically in the document. All have different features, but you

can see that quite a few of them have what is called TIF, Tax Incremental Finance. There is no

French term for it.

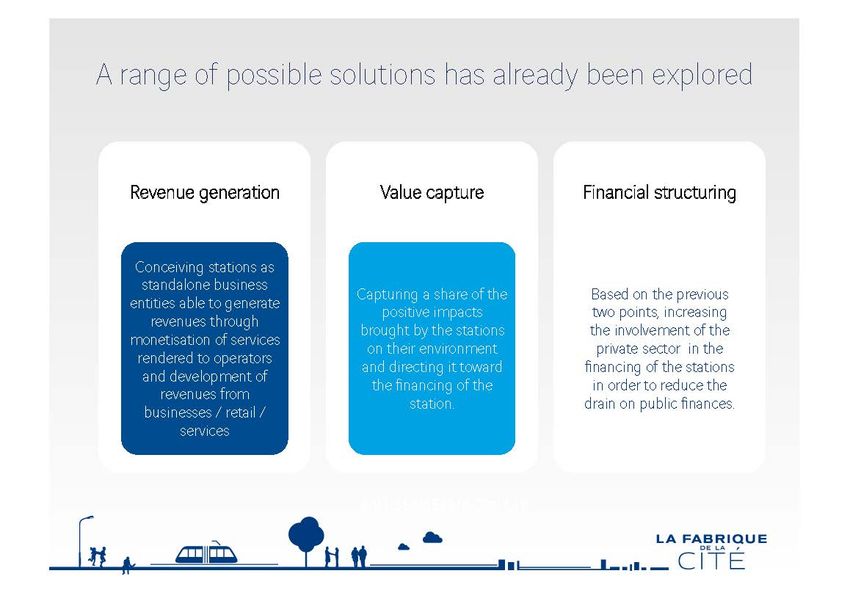

There are a couple of sources of revenue when you are looking at developing a station that are

outside the public sector's direct investment. You clearly get public sector support in a station, but of

the three sources of finance I would like to emphasise, the first one is capital contributions from

developers.

Now, you remember when I took a step back, I said there are no significant station

developments I am aware of that have not involved real estate development in the surrounding area

or above the station. The first point there really is that what traditionally happens when you are

developing these stations and you have got some land capture around there, you tend to try and

pick up a capital contribution from the developer in the area.

There are a couple of examples. Andrew Macdonald, works for Transport for London as

Corporate finance Manager based in London. He has worked on two station developments in

5

London (Canary Wharf and Vauxhall, Nine Elms and Battersea). He can give his thoughts. I guess

the most important thing from the experience in London is that TfL, as the station developer, is trying

to extract value from the property developers in the area.

I cannot quite remember the exact numbers, but for those of you that have travelled through

Canary Wharf in London, the business district, there is a new Crossrail station being developed that

you may have seen, although it is on the outskirts of Canary Wharf. The group that runs Canary

Wharf is a property development that have contributed I think £200 million to the development. We

can check that number. There is another station being developed in London at the disused power

station, Battersea Nine Elms. The Malaysian developer there is going to contribute about £200

million as well.

If you look at areas such as the Mass Transit Authority in Hong Kong, they adopt a

different model when it comes to development. This is in the case study. The city gives them

the rights for new lines and the rights for all the property development along the line. MTR take over

all the property along the railway line and they pay the city a nominal rental amount. Then MTR

takes the development profits on the line. Before railway station, after railway station, property value

increases and that is captured by MTR, the railway developer. These are alternative ways of doing

the same fundamental principle, which is extracting rent or charges from the private sector

developers in the area. That is the first point.

The second point I wanted to cover around value capture is the tax increment financing principle.

Tax increment financing is not new. It has been around for many, many years. I would guess it

started in the United States with some of the municipal bond initiatives, where at city level, they

borrow money. Tax increment finance basically has one particular form and a second example.

6The first form of tax increment finance is your property rates, and I expect you pay property rates

as business people in Paris as well. Tax increment financing gives the city a right to levy a

special surcharge, an additional amount above the existing property rates. That surcharge is

securitised and given to the developer of the infrastructure in the area to use as a contribution to

their infrastructure.

We have touched on capital contributions. Through the case studies, you will see that, and this

is an unfortunate fact of life, most of these instances normally have an additional special tax that is

levied on businesses and sometimes residential users in the area around the station or around the

railway line as well.

There are basically three sources of finance - capital contributions, tax increment finance

and special taxes. We have seen very, very few examples, if any - I have not seen any - of where

you can develop a station 100% with pure private sector capital. You need a combination of

public sector capital and private sector capital, and you need to put them in combination in

the private sector sources. To summarise, we have capital contribution, tax increment finance and

special taxes.

The final part just talks about financial structuring, and that is more a question of how you

bring all this together into a single financing vehicle. That is commercial structuring and legal. It

is not as important as the sources of the financing themselves.

I said I would go through a couple of case studies. There were nine that you saw. As I say, you

have got the detail in your books. I will touch on two. One is Potomac Yard and the other one is the

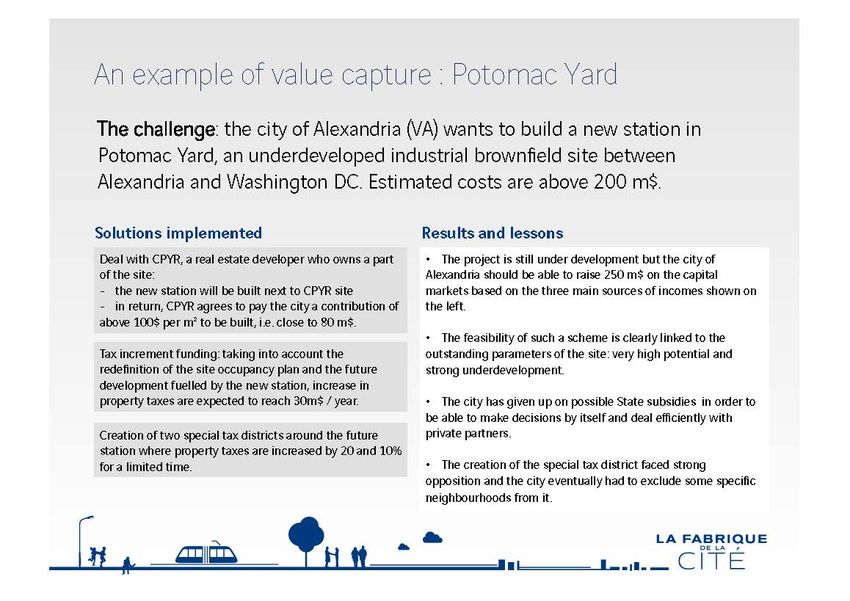

7refurbishment of Prague station. Potomac Yard is an area south of Washington DC. For those of

you who have been through Washington DC, it is about five kilometres south of Ronald Reagan

Airport, which is a small domestic airport that serves the city. You see planes taking off quite close

to the city centre, and that is Ronald Reagan Airport. If you really want to learn more, it is about 10

kilometres away from the White House, so it is just high enough that they will not get shot down

when the planes take off.

Nevertheless, it was a brownfield site, heavily, heavily contaminated. There was lots of pollution

because it was previously an industrial site. The city spent a lot of money decontaminating the site.

They wanted the developers to provide more residential and retail space in the area. One of

the key issues, as you can imagine with any residential development, a little like Battersea Nine

Elms, is that you have got the land, but you do not have transport access there.

The fundamental idea is to provide transport access through the form of light rail or urban heavy

rail services. It is quite interesting. They went to the public sector, to the federal government and to

the unique government that is Washington, DC, which I guess technically is a state government.

They asked them for money. Alexandria decided that it was not worth taking the federal money.

They did not feel that with all the conditions associated with the money, it was worth doing. It is not

often in life, in my experience, that you turn down money when you are a property developer or

when you are developing infrastructure, but in this case, Alexandria said, 'No, we are not going to

take the money.'

They tried to look for a pure private solution. CPYR is the development company that is

taking forward the residential development. The real estate developer wanted a new site there.

They were prepared to contribute about $80 million to $100 million to the development, not of the

8property because clearly that is their responsibility, but to the development of a station that would

bring residents and commuters to their area. That works out at about $100 per square metre. I do

not know what property prices are like in Paris. $100 per square metre is quite a lot of money. That

is quite a surcharge to impose on property development, but that is what they paid.

I have seen numbers, and Andrew may comment on this later. In our research, there was talk

around Battersea Nine Elms of the surcharge per square metre being £425. Does that sound about

right?

Andrew MACDONALD

It does sound about right, yes.

Richard ABADIE

It is astronomical. Do not buy property in London at those prices. What you are seeing there is

quite a wide range of surcharge that is imposed upon property development. We have $100 per

square metre and about £400 a square metre in London as a surcharge on a property. I do not

know what property costs per square metre in that particular area of London, but £400 is quite a lot

of money. Clearly, if a developer is not prepared to do it, they will not get the railway station, so it is

non-negotiable. In the Battersea Nine Elms example, it is absolutely necessary to get the asset

built.

Potomac Yard is about $100 per square metre, with a contribution of $80-100 million coming

from the developer. The tax increment financing we talked about will be the property

surcharge, the increase in property taxes that will then be securitised to pay for the area, and

then I also mentioned the special taxes, which is the sting in the tail. In this case, they created two

9special tax districts and are going to levy additional taxes. You can see that in this case, property

taxes are increased. That is when they build a future station. There are future revenues coming on

stream as well.

The result of all of that is that they are able to raise about $250 million to contribute towards the

station. It is a fantastic site, so this makes it a little bit easier in terms of development. That is the

one other feature I would say - when you are looking at greenfield station development and you want

to rely on real estate, clearly you have got stations that are very, very accessible to major city

centres. There is no point in building a very big station in the middle of the countryside because you

are not going to get people to live there. You need it to be attractive, close to the city,

commutable and in an appealing area for people to live.

I mentioned the third bullet, which is the city gave up on support from the government because

they did not want to deal with them anymore. That is actually another thing that I would emphasise,

and it is a statement again of the obvious. Taxes are not popular. Increases in property taxes

are very unpopular. Special taxes are even worse.

One thing you need is if government is going to commit to building some of these stations, they

are going to have to accept if they do not pay for it through the general tax base that they have and

the only solution is to levy surcharges and taxes upon residents in the area, it is going to be

unpopular. If you are the mayor of a city, do not expect to be re-elected on the back of your

message, which is, 'I have raised taxes.' Try and make sure you get the station built before the

taxes kick in. That is a bit of an aside there. That is one example.

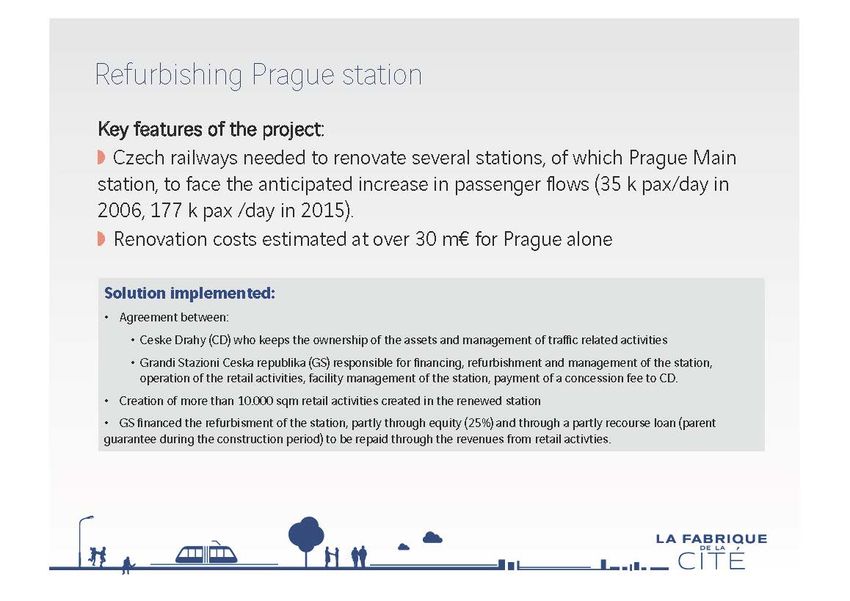

The second example is slightly different. Prague station, as you can imagine, has already been

built. It is an existing station. This was more a refurbishment of Prague station, which is another

fantastic masterpiece. Grandi Stazioni, which is the concessionary for the refurbishment, is a public-

private partnership. It is 60% owned by the railway company in Italy and 40% of its shares are

owned by the private sector. I think SNCF have a minority stake in it as well, so there is a mix of

shareholders. It is not just the Italian state-owned rail company doing it - it is a joint venture in its

own right.

10The key thing is that they were able to raise money to refurbish the station, create some

more retail space, and that is another important point that I will talk about a little later. Retail

revenues from station development are very important. They are not as important as you would

think though. They do not throw up so much additional revenue that you can clearly build a station

in its own right. It is supplemental revenue.

When I went through Delhi station, trust me, I did not want to buy any of the food there because I

am sure it would have been contaminated. It is an awful station. If you get the aesthetics of the

station right, you can turn it into a shopping centre hub principle. It is actually quite dangerous, and

this is probably not the right point to say, but I will make the point anyhow. I had recently been

through Warsaw station and Krakow station. For those of you who have visited Warsaw and

Krakow, the stations are quite old. They are run by a state-owned company. They are not great to

travel through, but interestingly enough, because the public sector state-owned rail company in

Poland was not prepared to redevelop the stations, the private sector property developers took the

initiative to build massive shopping centres right next to the station.

When I walked out of Warsaw central station, I walked straight into a shopping centre, and it is a

great shopping centre. If I wanted to buy food, drink, shoes, cameras, anything, I would walk into

the shopping centre right next to the station. Warsaw station and the public rail company in Poland

do not make one cent or one zloty out of the property development. The message in there is that it

is all fine saying you do not want to invest as the state-owned railway company, but if you do not

invest, some entrepreneurial private sector property developer is going to do it for you and you are

not going to get a benefit from it.

When you are looking at a retail development like in Prague station, one of the objectives

is to raise revenues either for the state or for the rail company, rather than to have the private

sector take those revenues outside the station. These are just two examples of the

refurbishment that has taken place. I have been through this already. I have talked about the tax

11incremental finance and I have talked about the capital contributions that come from joint property

development.

An example of joint property development is the Crossrail station in London. It is the

Canary Wharf group, which is the real estate owner in Canary Wharf, doing a joint venture with

Transport for London to jointly develop the station. There are joint property development

agreements where the public sector will develop it, but there will be contributions from the

developers of the real estate.

There are more details in the hand-outs that very briefly touch on some of the benefits of what

we have seen with tax incremental finance. What I will focus on for now is just the three red bullet:

• Direct proximity with highly developed areas (Potomac couple of miles away from the

White House, Hudson in the middle of Manhattan...);

• blatant underdevelopment compared to surroundings (typically brownfield industrial

sites);

• public policy permits hypothecation of rates/taxes

TIF is successful with direct proximity of highly developed areas. My earlier point is that

you can only really make money if it is somewhere people want to travel to and somewhere that you

can actually impose surcharges on property development and surcharges on property rates where

people actually want to live. If people do not want to live there, you are not going to make any

money out of the tax increment finance.

We talked about Potomac being close to Washington Central. For those of you who travel

through New York regularly and for those of you who have visited the Intrepid, the aircraft carrier that

sits out on the Hudson River, the Hudson development area is just south of the Intrepid, and that is a

massive new redevelopment in Manhattan. There were again no metro services, so therefore the

area was dilapidated. That has been redeveloped and they are building Line 7 to extend through

Hudson, so that is a massive property development area as well, following some of the principles we

have talked about.

Again, another development point is that you have got to pick brownfield sites that have

traditionally been industrial sites because that tends to be where you get a lot more development

taking place. Examples are the docks in London or power stations in London or the Hudson area,

which used to be rail marshalling yards. Rail traffic historically was these underdeveloped areas.

The third bullet there is very important (public policy permits hypothecation of rates/taxes). In

the UK, for a long period of time, the Treasury said that they would not allow authorities to ring-fence

revenues to keep for themselves. The Treasury felt that all taxes that are imposed belong to the

Central Treasury, so it required a shift in mindset, a shift in policy in government to allow for the ring-

fencing of these revenues. If you cannot ring-fence them and you cannot dedicate them, then there

is no way you can use tax incremental finance.

I have talked about Hudson Yards. For both Hudson Yards and Battersea Nine Elms extension,

I would say that whilst the revenue has been identified, the revenue has been securitised, that has

not been enough on its own to get the projects going. In the case of Hudson, the City of New

York has had to guarantee that if the project company cannot repay the interest on the debt,

the City of New York would step in and repay the interest. There is a guarantee from the City of

New York.

In the case of London, for the Battersea Nine Elms extension, we understand that at the

moment, there is talk of the Central Treasury guaranteeing that if the property rates and revenues do

not materialise, they will underpin them and guarantee the minimum. There is always some

form of additional intervention from government for the very, very big projects. Hudson Yards was

about $3 billion and the Battersea project is about £1 billion, so these are significant projects in their

own right, hence the need for additional intervention.

12Louis-Roch BURGARD, Président, VINCI Concessions

Is the whole risk guaranteed by the public authority or is it just part of it ? There is a wide area of

revenue.

Richard ABADIE

In Hudson Yards specifically, as I said, tax incremental funds is quite well understood in the US

in the form of the municipal bond market. They have done exactly the same thing. They have

created what is called a revenue bond, which means that the buyers of the financial instrument rely

not on the city to repay them, it is not a general obligation of the city, but an undertaking from the

project. Normally what happens with revenue bonds is if the project does not repay you, you as the

lender to the project lose your money.

The buyers of these bonds for this particular project at Hudson Yards said it is a new greenfield

project in an area that is unproven. Nobody wants to live there. Just to give you a perspective,

property prices in the Hudson area are 50% lower than the rest of Manhattan, so it is an area

nobody lives in. The people that do live there you probably do not want as neighbours if you are

living in New York. The problem there is that none of the lenders or the investors in the bonds felt

that they could afford to take the risk of seeing that area change over time, so the anticipated growth

in revenues was about 4% a year. I think the payback period is about 50 years.

The investors in that market were not comfortable with this. This is really real estate

development. They were not comfortable taking the real estate development risk. The only

guarantee they asked for was not a guarantee that in the event of termination, they get repaid - it

was just that when interest is due, it is then repaid, which is a very narrow guarantee. It is still a

revenue bond, but with one specific obligation.

On the TfL Battersea Nine Elms example, that is still under development. I am not sure where

that is going. I think the negotiations continue.

Philippe BOZIER, Directeur de projet, Finance & PPP, PwC

As far as I know, the Battersea project is not just a station, but the extension of the line.

Richard ABADIE

Correct. That is absolutely right. I cannot remember the exact numbers, but there are two

stations and there is also the railway line itself. Some of that obligation will clearly be picked up by

TfL themselves, not just by the special purpose vehicle of additional contributions.

My last point is that some of the development that takes place is not only around

brownfield sites and residential development around stations - it is around the area above the

station as well. We are increasingly seeing railway stations where the air rights above the station

are being sold for residential developments. In the case of Canary Wharf in the UK, the Canary

Wharf group made its capital contribution, but they reserved the right to have four floors of retail

development above the station itself, so that is how they were going to get paid back. They took a

head lease on the four floors and then they rented it out again, a little bit like MTR does in Hong

Kong.

Regarding the main findings around revenue generation, I made the point that it is possible to do

it. The last point there is very important. Commercial activities, retail and rental will not pay for a

station, particularly a greenfield station in totality. You still need a public sector contribution to these

stations as well. It is meant to be a PPP (Public Private Partnership) or joint venture, rather than a

way of the public sector not putting any money into station development.

We took all these nine stations. We did some maths on them and we can have a debate as to

whether they are accurate or not, but what we are saying here is that, and I have to get this right, the

average investment in stations was about €20 million a year. The average number of passengers

was about 20 million passengers a year.

13Now, when I say the average investment was €20 million, that was sort of the maximum amount

that could be supported by the number of passengers going through there. Looking at that from a

retail point of view, and I am not saying you directly charge your customer €1 per year, but the

theory varies. If you have got a 20-million passenger station, you can afford to extract about €20

million from the through traffic and from the property development through the retail and rental

process. It is basically EUR1 per passenger per year. If you go above that, you tend to find that the

contribution will have to be paid for by alternative means. It is a very, very rough rule of thumb.

Then the second point is just around the amount of retail space that you can have per

passenger going through there. I would not look at that very scientifically, but let us say eight to

nine passengers per square metre of retail space. If you have more retail space than passengers,

you are not going to make it a profitable business. Those are very, very rough, based on some of

the research that we have done.

Consultation with external parties is the last point there. It is quite important as well. Both those

projects struggled and the reason was because the public clearly did not want to pay the additional

cost to them and there were political concerns about re-election. Therefore some special deals were

cut. If you are trying to raise money for your stations, it is not something you can do very quickly. It

requires a lot of debate and discussion with the political parts of government.

Thank you very much.

14Discussion

Andrew MacDONALD, Corporate finance, Transport for London

Canary Wharf and Crossrail are in fact two stations in itself plus the railway line. I think Richard

has gone through the topic and covered it very well. I think from TfL's perspective, I would draw out

that when funding any station or any large project, with each of these different tools, such as using

TIF, contributions from private developers, whatever you use, you will always invariably find that one

tool is not enough.

In particular, when we looked at Crossrail, which admittedly is a mega project, we got £150

million from Canary Wharf for a £500 million station. The other £350 million came out of a general

Crossrail pot, a third of which was funded from grants, so from general taxation; a third from debt

that was raised against future revenues. We are lucky that Crossrail is a very profitable line. If you

do not have a profitable line, that source of funding clearly will not be available to you. The final third

was from business rates, which is a form of tax incremental finance. I think the important thing is

that you will find that you will have to blend all of the different tools in different measures to be able

to deliver any project.

The other thing that I would draw out, and Richard mentioned this, is regarding TIF. In some

ways, TIF is quite a difficult tool to use because the development risk is absolutely key since it

affects not only whether or not you get the funding, but it affects the timing of the funding as well

because you are dependent on how quickly the development comes to market and how quickly the

incremental finance can be drawn out. I thought it was very interesting to hear the results of your

study, so thank you very much. I am happy to take any questions on either of the two TfL stations.

Dans l’expérience de TfL, il ne suffit pas de recourir à un seul outil de financement. Dans

l’exemple de Woolwich Crossrail, nous avons contribué à hauteur de 150 millions de livres sur un

total de 500 millions. Le reste provenait d’un « pot commun » monté par Crossrail constitué pour un

tiers de revenus fiscaux, pour un tiers de dette levée contre les revenus futurs et pour le tiers restant

de droits commerciaux, c’est-à-dire une forme de taxation. Il faut recourir à un ensemble de

différents outils pour assurer la réussite d’un projet.

Deuxièmement, le TIF est un outil difficile à manipuler : le risque de développement est

prépondérant. Il affecte non seulement le financement lui-même, mais aussi le calendrier de

financement : on dépend de la vitesse à laquelle le projet arrive sur le marché et de la vitesse à

laquelle les financements supplémentaires arrivent.

Alain MEYERE, Directeur du département Mobilité et transport, IAU IDF

L’exposé montre que les outils ne sont pas adaptés à toutes les situations. Le TIF consiste à

utiliser des recettes fiscales supplémentaires pour rembourser des emprunts, or on se trouve

souvent dans une situation où l’on ne maîtrise ni le montant des recettes, ni le calendrier de rentrée

de ces recettes. Cela fait peser un risque sur l’opération. Comme le dit Andrew MacDONALD, il faut

recourir à toute une batterie d’outils pour éviter ce risque. Plusieurs développeurs se sont ainsi

attelés au projet de Battersea Station et ont fait faillite successivement, ce qui a pesé sur le

prolongement de la ligne de métro.

Il en va de même pour le métro de Copenhague. On a d’abord pensé le financer par la vente

des droits de construction et par les recettes fiscales générées par la construction d’une ville

nouvelle dans l’immédiate proximité de l’aéroport. Or la commercialisation de cette ville nouvelle ne

s’est pas du tout passée comme prévu, notamment en raison de la concurrence sur le marché de

l’immobilier de la rénovation du port de Copenhague. Le calendrier de remboursement n’a donc pas

pu être tenu.

Pour conclure, les outils sont intéressants mais ne peuvent être utilisés que pour

certaines gares. En d’autres termes, il n’existe pas de solution universelle qui s’appliquerait

par exemple à toutes les gares du Grand Paris.

15Louis-Roch BURGARD

L’exposé a bien montré qu’il fallait utiliser plusieurs solutions. En matière de calendrier,

l’important pour les prêteurs est d’avoir la garantie du service de la dette. Richard Abadie a confirmé

que cette garantie avait été apportée. Les problèmes de timing subsistent mais sont beaucoup

moins sensibles, car le risque de défaut a disparu.

Philippe BOZIER

Hudson Yards est l’exemple typique d’un site sous-utilisé, dans une localisation extraordinaire.

C’est le seul exemple que nous ayons identifié d’un projet intégralement financé par un mécanisme

de TIF. Le financement se fait sous forme obligataire. La garantie de la ville de New York porte sur

les intérêts et permet de rassurer les prêteurs vis-à-vis des retards. Le premier promoteur

sélectionné pour Hudson Yards a effectivement fait faillite, entraînant deux à trois ans de retard pour

le projet. La garantie a donc été activée.

Remi DORVAL

Ma question porte sur le phasage non pas des travaux, mais des décisions. A-t-il fallu des

décisions successives, opération par opération, ou le projet a-t-il fait l’objet d’une décision globale

sur un territoire initial, servant ensuite de support au montage du financement ?

Richard ABADIE

The decision to use Tax increment Financing (TIF) is difficult. It takes a long time to get past

some of the political objections to the hypothecation of revenues. My experience is that developers

of new railway lines, and often stations, who want to use Tax increment Financing will not be looking

only at Tax increment Financing; they will be exploring multiple sources of solutions.

However, they cannot wait to exhaust all the others and then look at Tax Incremental Finance. It

is something that has to be done in parallel. Coming back to your point, it is not done in stages; it is

done upfront, exploring all the options. If it is a realistic option, you get the Treasury approval. You

get the political buy-in to increasing property rates in the area. Then you can go through the public

consultation and implementation process.

I cannot remember how long it took on the Battersea Nine Elms development; it was relatively

short. However, you can look at many of the property developments, even something like

Canary Wharf. It is not in our case study, but if you go back far enough in Canary Wharf’s history, it

used to be a disused seaport, with stock yards. The initial Canadian developer of Canary Wharf

went insolvent.

It did not go insolvent, because of TIF not working; it went insolvent because it is a

property development, at the end of the day. Property developers all over the world suffer as

property markets go up and down. They were not exploring Tax increment Financing. It was only

when the Canary Wharf Group took them over that they explored the Tax Incremental Finance and

the developer contributions. It is the same thing on the Battersea Nine Elms example; it is the same

thing in the US.

I have a warning in relation to France in particular. As one gentleman mentioned, you have not

done it before. If you have not done it before, it is going to take a long time to socialise it and to get

it accepted by the various authorities. If you are looking at it for Grand Paris, it is something that you

almost want to start now. You need to develop the idea, because it is going to take some time to get

approved, if it is ever approved.

La décision de recourir à un TIF est difficile et exige un certain nombre d’exigences pour

surmonter les obstacles politiques à l’hypothèque des revenus. Dans mon expérience, les

développeurs de nouvelles lignes ferroviaires et de nouvelles gares explorent plusieurs pistes. Il est

toutefois très important d’envisager toutes les solutions en amont et de front.

Je ne me souviens plus exactement du temps nécessaire pour parvenir à la décision sur ligne

Battersea Nine Elms. Il est resté relativement court. Dans l’exemple de Canary Wharf, il s’agissait

d’une zone de docks abandonnée, dont le promoteur initial a fait faillite pour des raisons de

16promotion immobilière à proprement parler. Dans le cas de la France, il est important de lancer les

idées suffisamment en avance pour les faire accepter par l’opinion publique.

Thierry PONTILLE, Directeur de projets, VINCI Concessions

L’étude n’a pas abordé les coûts de maintenance et de mise aux normes. Une gare est un

établissement recevant du public, qui exige des réinvestissements réguliers au long de la vie de

l’ouvrage. Les recettes générées par le commerce et les taxes permettent tout juste d’équilibrer les

coûts de maintenance, et donc ne contribuent pas au financement de l’infrastructure.

Philippe BOZIER

Le sujet de la maintenance est partiellement couvert dans les exemples de gares à activité

commerciale que nous avons étudiés. On observe généralement une répartition des tâches entre

opérateur ferroviaire et concessionnaire privé. Dans plusieurs exemples de gares italiennes, le

concessionnaire assure la maintenance quotidienne et les petits renouvellements sur l’ensemble de

la gare. Les revenus des activités commerciales peuvent répondre partiellement au problème, mais

ne permettent effectivement pas de mener les grands renouvellements après trente ans.

Pierre LACOMBE, Directeur stratégie et finances, Gares et Connexions

Cette étude de comparaison des gares est très intéressante, mais ne porte que sur de grandes

gares avec un potentiel commercial. Or le plus grand projet de renouvellement en France porte sur

l’accessibilité, obligatoire à partir de 2015. Le plus grand projet actuel est de 1,3 milliard d’euros et

concerne 400 gares en Ile-de-France. Le potentiel commercial est inexistant : le financement se fait

en partie sur fonds propres des opérateurs et pour le reste sur fonds publics. Le projet de Juvisy

représente par exemple 100 millions d’euros, dont 15 % à 20 % pour la gare. Les trois quarts de

l’enjeu concerne en effet le rehaussement des quais, et pour le reste, la réalisation des escalators

ou des rampes. Le cas est donc très particulier.

En Europe continentale, le principal contributeur est l’opérateur ferroviaire, soit en raison d’un

péage spécifique aux gares comme en Espagne, en France ou en Allemagne, soit directement sous

forme de péage aux infrastructures. Or le principal opérateur ferroviaire est souvent l’acteur

historique.

Une gare peut être considérée, comme cela a été dit, comme un établissement recevant du

public. En Allemagne par exemple, les quais sont financés par le péage, les autres équipements

étant financés par des développements commerciaux. Suivant les pays, la solution passe par des

subventions ou par le financement du gestionnaire de gares. En France, la Ville de Paris et la

Région s’intéressent peu à ces grandes gares. Les opérations de Gare du Nord ou de Saint-Lazare

n’ont donc pas été faites sur deniers publics. Le projet porte essentiellement sur le bâtiment et non

sur les lignes ferroviaires. Le financement est beaucoup plus public ailleurs.

Yves-Thibault de SILGUY, Vice-président du conseil d'administration et administrateur

référent, VINCI

Les gares appartiennent pourtant à la SNCF en France. Est-ce le cas dans les autres pays ?

Cela ne complique-t-il pas les problèmes de financement ? Si il y a qu’un seul propriétaire, la SNCF,

pourquoi mobiliser les autres potentiels financiers ?

Pierre LACOMBE

Les gares appartiennent à plusieurs propriétaires en France. Les quais longitudinaux et les

équipements connexes (passerelles et souterrains) appartiennent à RFF et l’ensemble du bâtiment

à la SNCF. Le foncier de la gare est donc éclaté et tout projet donne lieu à de longs débats sur la

responsabilité de la maîtrise d’ouvrage.

Yves-Thibault de SILGUY, Vice-président du conseil d'administration et administrateur

référent, VINCI

Cela ne change rien, car RFF est un démembrement de la SNCF.

17Pierre LACOMBE

Cela change en réalité beaucoup de choses. L’extérieur est tout aussi éclaté, or l’essentiel de la

valorisation dans un projet, comme à Lyon Part-Dieu, se fait à l’extérieur de la gare, zone qui

appartient souvent à la ville et non à la SNCF ou à RFF. La question est comment on fait rentrer cet

argent dans ce projet de gare ?

Louis-Roch BURGARD

La dépense par passager est beaucoup plus élevée dans les aéroports que dans les gares.

Comment l’expliquez-vous ? Comment augmenter la recette par passager ?

Deuxièmement, y a-t-il un exemple en France de projet parvenu à créer une unité dans et autour

de la gare pour générer de la recette additionnelle ? On peut investir sur la rénovation d’une gare, et

voir les profits, aller aux habitants alentour et la ville, qui n’ont pourtant pas contribué.

Richard ABADIE

I will deal with the first question, because the second question is not for me. It is interesting. I

have got to travel back to London now through Gare du Nord and it is not a particularly pleasant

experience as a traveller. I know there are retail facilities, but they are away from the area you

would normally walk through. However, you arrive at St Pancras on the Eurostar on the other side.

What I was just saying is that I have now got to go back to London through Gare du Nord and

through St Pancras. As we all know, St Pancras has been heavily redeveloped. The one thing

about St Pancras is that you have to walk past the retail facilities; you cannot avoid them. You may

want to avoid them, but they are going to be there. One of the reasons for that is that the station

refurbishment was designed along that basis; you cannot avoid them. I do not think that when Gare

du Nord was redesigned, it was designed on that basis; I doubt it.

There are lessons that have been drawn. I like your comparison to airports. The concept that is

increasingly being talked about in the airport sector is airport cities. The airport is a hub for

passengers flying around the world or wherever they are going. However, more importantly, it is

meant to be a city in its own right. It is going to have hotels; you can sleep there, you can shop

there. You can do everything.

The difference between an airport and a railway station is that normally the commuters at railway

stations are commuting relatively short distances. They are normally in a hurry to get to the office or

to get home. They do not stay at the station purely for the sake of the station; it is normally a path

through. Now, the closest I have seen recently to an airport city in a railway station is the Stratford

Station next to the Olympic Village in London. I do not know which of you has been through there. I

think it has the largest shopping mall, at least in the UK. It is called Westfield; the property

developer built a very big shopping centre.

It is the same thing; you come out of the Stratford station; you have to walk through the shopping

centre. Some people will say that is a bad idea; they would much rather not walk through the

shopping centre. However, the interesting thing is that it is a partnership between the property

developer and the railway station. The benefit to the property developer is that people going home

in the evening are doing the shopping on their way to the train. Clearly, they do not want to be

carrying big bags. However, they may want to buy a new shirt or a light dinner for the evening.

They may have forgotten to do some of some of their grocery or retail shopping because they were

working during the day.

There are brand-new station developments which are big hubs: not the small stations as you are

re going through the suburbs, but the big new stations. These are going to have to adopt those

models in the future. They have to be integrated places that people will go to and stop over.

You may be meeting a client before you go home for the evening, I know people who travel

through Stratford will meet in the shopping centre, because the railway station is two minutes away.

You do not have to worry about catching a taxi to the railway station. It is becoming a centre where

people will go, not necessarily to end or start their journey; there will be other activities that take

18place in addition to it. This is because you have got retail, food courts, restaurants and everything

else.

I tell people around the world that if you are looking for big new stations in the UK, it is how

major train stations are going to be developed in future. It is a combination; it is a railway city, if we

want to draw the comparison to the airport cities. The key difference between an airport city and a

station city is the amount of time passengers at the airport will spend at the airport. In a railway

station, a large number of people are just passing through.

They may stop. I will give a little example. I do not know what it is like in Paris, but if you go to

most big railway stations that have been redeveloped, there are no seats. If you go to some

stations, you can sit, but these days you do not have seats. Why is that? It is not because the

developer does not want you to be comfortable; what they want you to do is to shop. They want

you to walk in; you cannot sit, so you will walk in and buy a newspaper, a drink or something else.

The way the stations are being configured is around the retail experience, to try to

maximise revenues. As a customer, it is quite convenient for me, if I am heading home in the

evening, to be able to do some of that. When I came here, I did not bring a tie with me, so when I

was at St Pancras, I quickly popped into the tie shop to buy myself a tie. That is the type of

convenience I need, rather than going somewhere else to try and buy that stuff.

Les aéroports sont conçus comme des villes en soi : on peut y passer la nuit, s’y restaurer ou y

faire du shopping. En revanche, les gares ferroviaires sont des lieux de transit.

La gare de Stratford, à proximité du village olympique de Londres, est le plus vaste centre

commercial britannique. En arrivant à la gare, on passe devant les commerces pour parvenir aux

quais. Inversement, les voyageurs font leurs courses au centre commercial avant de prendre le train

pour rentrer chez eux. L’avenir des gares passe probablement par ce modèle : elles doivent être des

centres intégrés, un peu comme les aéroports, sauf que les voyageurs passent beaucoup moins de

temps dans les gares que dans les aéroports. Dans beaucoup de gares britanniques, on ne peut

pas s’asseoir, par exemple : il ne s’agit pas d’empêcher les personnes d’être confortables, mais de

les pousser à passer du temps dans les espaces commerciaux.

Francesco GARGANI, Executive Director, Government Services, PwC Italie

I just have one or two words to say. The stations are places where people start their journeys.

These days, the station managers are actually designing their stations to force people to go through

specific parts of the station. They have to make sure that they get to the windows and that the flows

in the stations are good for the passenger movements, but also for the shops.

There is one example of a big station capturing the value from the area surrounding the station.

People are attracted by the station, not just because they go there to travel, but also because they

can do the shopping. We are seeing a lot of these facilities most of the time, from my personal

experience these days, working in Eastern Europe, which have huge potential for commercial

development inside. However, all the revenues were captured just outside the stations.

In some cases, there would be a big McDonald’s just next to the station and these are some of

the most profitable McDonald’s in Europe. They are able to position themselves in a cheap way,

because there is availability of commercial space just outside the station. People use the station just

for travelling, but not really for shopping.

I think that the key for a station manager in developing a station is to integrate such concepts

within the station, to maximise the space per square metre. It is feasible, because it is possible to

attract people from outside. A dialogue has to happen between the station manager, all the people

participating in the project and the local authorities. It is important that concessions or agreements

are given for re-allocating space from the outside of the station to the inside.

Les gares sont des lieux où le public commence sa journée. Elles sont dessinées pour canaliser

le flux des passagers à travers différentes zones à l’intérieur de la gare. Les gares peuvent alors

devenir des zones commerciales. Beaucoup de gares en Europe de l’Est ont un potentiel important,

mais il est exploité dans la zone immédiatement adjacente. Les McDonald’s européens les plus

19profitables sont par exemple situés immédiatement à l’extérieur des gares. Il est donc important pour

le gestionnaire de la gare d’intégrer les concepts pour maximiser le revenu par m².

Pierre LACOMBE

Les aéroports de Paris drainent 80 millions de passagers par an, contre 130 millions pour la

gare Saint-Lazare. Le potentiel est donc considérable. Le fast food de Montparnasse fait le même

chiffre d’affaires que celui des Champs-Elysées. Le jour de l’ouverture, les revenus au m² à Saint-

Lazare étaient plus élevés que dans les grands magasins voisins.

Sur le deuxième point, la réforme du ferroviaire est peut-être l’occasion de travailler sur la

réunification du foncier entre les différents opérateurs.

Amélie FIGEAC, Directrice administrative et financière, EPA-ORSA

L’aménagement par les rentrées fiscales est un enjeu majeur. Nous travaillons sur d’anciennes

zones industrielles où le foncier reste très élevé, au point qu’il est difficile d’équilibrer l’opération

d’aménagement si l’on y inclut la gare. Ensuite, la fiscalité sert à financer le fonctionnement courant

de la ville. Capter les retombées fiscales pose donc un problème d’équilibre des comptes locaux.

Nous sommes un établissement public d’Etat. Notre mission est d’accroître l’offre de logements,

mais les collectivités avec qui nous travaillons veulent des activités et des bureaux pour des raisons

fiscales : elles ne peuvent pas fonctionner uniquement sur des rentrées fiscales de logements. Cela

suppose un marché de bureaux alentour, alors que celui-ci est très déprimé à l’heure actuelle.

Christophe GARAT, Directeur délégué à la refonte du système ferroviaire, SNCF

Je travaille sur la réforme ferroviaire. Nous réfléchissons avec RFF sur la possibilité de mieux

valoriser le potentiel foncier qui est très important, et pour l’instant, éclaté selon des règles

totalement incompréhensibles. Nous sommes convaincus que le potentiel est très important sur des

zones encore classées en activité ferroviaire mais qui n’ont plus réellement d’utilité aujourd’hui.

Nous voulons les rendre à nouveau exploitables. A ce sujet, le premier problème est de parvenir à

une unité juridique pour la propriété. Nous espérons que la réforme permettra de mettre en place un

système foncier plus raisonnable qu’à l’heure actuelle.

Eric VEILLARD, Chef du service, Gares de voyageurs, Direction du Foncier et de

l'Immobilier, RFF

Le sujet foncier entre les deux établissements publics ferroviaires est complexe. Au-delà de

l’intérêt urbain de ces emprises se jouent également des enjeux ferroviaires. Une grande difficulté

est de préserver les emprises foncières. Il est important de pouvoir réserver des capacités sur des

échelles de temps très longues : une fois que le foncier est vendu, il est impossible d’y revenir. Le

problème se pose de manière cruciale par exemple à Saint-Lazare, où il est impossible d’allonger et

d’élargir les quais.

Nous essayons de mutualiser nos emprises et d’avoir des approches globales vis-à-vis de la

collectivité. La difficulté est de rendre mutables les terrains, c’est-à-dire d’identifier des terrains

pouvant servir du giron ferroviaire, tout en préservant les activités : Paris-Gare de Lyon a par

exemple des problèmes de remisage d’exploitation. Par ailleurs, les valorisations foncières ne sont

pas réinjectées sur les sites en raison des règles de péréquation nationale. Nous le faisons dans le

locatif, car la loi nous impose de reverser, dans le péage, 50 % des recettes de valorisations

locatives des gares. Les valorisations foncières sont en revanche « fléchées » vers l’aménagement

des réseaux.

Philippe BOZIER

Le problème de l’éclatement ne touche pas seulement RFF et la SNCF. A New York par

exemple, la municipalité s’est approprié les prérogatives de la MTA et de l’Etat de New York pour

avoir un contrôle absolu sur le projet et le faire avancer.

20Vous pouvez aussi lire